Explore by category

Understanding reverse mortgage payout options

In this article:

- FHA Lending Rules: The 60% utilization rule for home equity conversion mortgages (HECM)

- Option 1: Lump sum payout

- Option 2: Monthly payouts

- Option 3: Line of credit

- Can you change the way you receive your loan proceeds?

- Which reverse mortgage payout option is best?

- How much could you be eligible for with a reverse mortgage loan?

Most traditional loans offer a one-time payment of proceeds—or, in the case of a HELOC, a line of credit. However, reverse mortgage loans work a bit differently. In addition to having distinct eligibility requirements from other loans, many reverse mortgages offer multiple payout options, including a lump sum, monthly payments, a line of credit, and, in some cases, the ability to combine different payout methods.

This feature allows borrowers to choose how to receive reverse mortgage proceeds to suit their financial plans and situation. This guide will explain the different ways borrowers can have their loan proceeds disbursed. But first, we need to explore the 60% utilization rule and how it might impact the amount you may be eligible for.

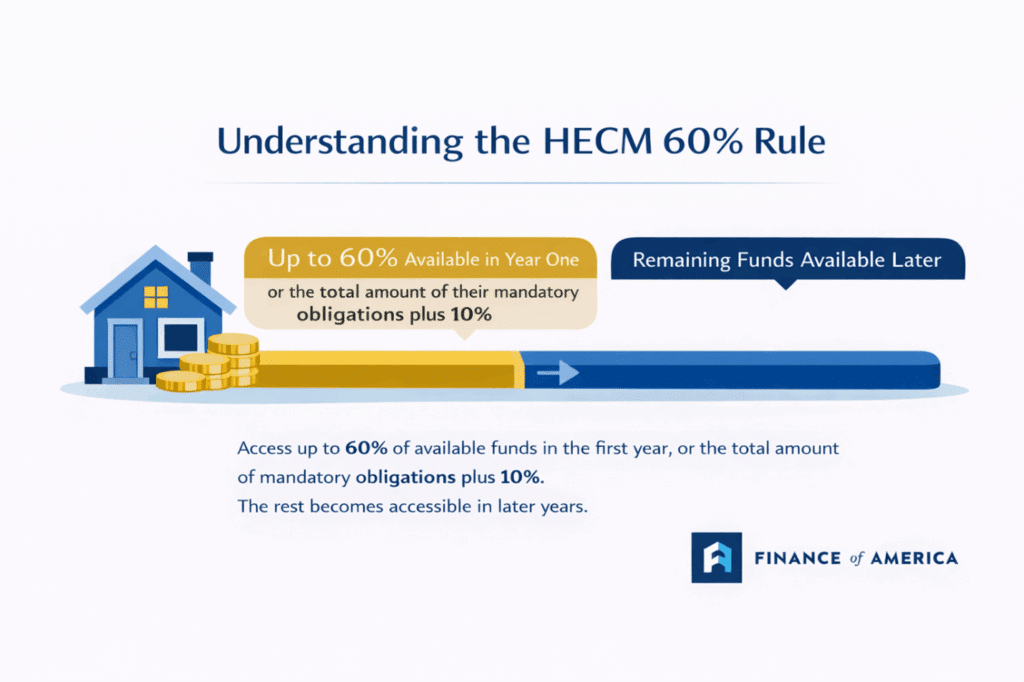

FHA Lending Rules: The 60% utilization rule for home equity conversion mortgages (HECM)

The total amount of available proceeds is determined by several factors, including the home’s value, the amount of equity in the home, and the FHA lending limit, which is $1,249,125 in 2026. Which means with a HECM, you can never take out more than $1,249,125. But there’s also the 60% rule.

The 60% utilization rule says borrowers who choose a home equity conversion mortgage (HECM) may only take the greater of 60% of their total available equity or the total amount of their mandatory obligations plus 10% in the first payout.

Mandatory obligations may include the balance of a traditional mortgage or other liens on the home. When calculating how much cash a borrower can take in their lump sum, the lender calculates the borrower’s mandatory obligations and adds 10%. They compare that number with 60% of the total available equity to determine how much a borrower can take in their first payment.

Let’s say you have $200,000 in home equity. The 60% rule means you can only access $120,000 during the first year. The remaining 40% can be accessed only after the first 12 months. This rule applies to all the disbursement methods we’ll cover in this article.

It is worth noting that this rule applies to all HECMs, which are the most popular type of reverse mortgage. HECMs are insured by the Federal Housing Authority (FHA) and must follow specific HUD (Housing and Urban Development) guidelines related to payout amounts and eligibility. Other reverse mortgages from private lenders, such as jumbo reverse mortgages, may have different requirements and limits on loan amounts.

These materials were not provided by HUD or FHA and were not approved by FHA or any government agency.

To learn more, please visit the CFPB’s Reverse Mortgage Guide.

Option 1: Lump sum payout

A lump sum payout means the borrower takes all their available equity as a single payment. This is similar to the way funds are distributed with a conventional home equity loan.

Under the 60% utilization rule, only a portion of the home’s equity will be available as a lump sum at mortgage closing. The loan structure will further determine how much cash borrowers can ultimately take out.

- Adjustable rate HECM: Borrowers can take the remaining 40% of their balance after one year.

- Fixed-rate HECM: Borrowers can only take the initial 60%, meaning the equity available with a fixed-rate HECM will always be less than the equity available with an adjustable-rate HECM. The lump sum option is the only payout available to fixed-rate HECM borrowers.

The advantage of a lump sum payment is that you can use it to cover large expenses all at once. However, the lump sum option generally results in the highest initial loan balance and the fastest interest accrual.

–> To learn more more about how reverse mortgages work, read our guide What is a reverse mortgage?

Option 2: Monthly payouts

Monthly payouts allow the borrower to receive a set amount from their available equity. The loan balance grows as they receive payouts, and interest is charged as they draw on the loan. There are two structures for reverse mortgage proceeds to be received as monthly payouts.

- Term payouts: Monthly payouts can stretch over five, 10, or 20 years or another timeframe that works for the borrower. Since the lender sets the exact term, the borrower’s monthly payout tends to be higher than the second monthly payout option.

- Tenure payouts: These payouts are designed to last the borrower for life. They will likely be lower than term payout because they need to cover a longer, less definite period. This option is available as long as the borrower lives in the home as a principal residence, pays property taxes and insurance, maintains the home, and complies with all loan terms.

Although no monthly mortgage payments are required, to retain ownership and avoid default, you will still be required to pay your property taxes, insurance, upkeep in a timely manner and comply with loan terms for as long as you own your home.

Deciding between a term and a tenure payout plan depends on the borrower’s financial strategy and other factors, including the amount of available equity and future plans. The benefit of this payout format is that it may offer stability; however, it can make paying for large expenses more challenging.

Option 3: Line of credit

A line of credit allows reverse mortgage borrowers to keep their available equity in reserve for a later date, similar to a HELOC. A unique feature of a line of credit with a home equity conversion mortgage is that the amount of unused credit available grows over time in relation to the amount of interest charged on the principal.

To keep a reverse mortgage line of credit open, borrowers must maintain at least a $100 loan balance. Any equity above that threshold can be put into a line of credit. The key feature of a line of credit is that it can remain untouched for years for borrowers to tap as needs arise.

This option provides the greatest flexibility to access the funds only when needed, which may preserve your equity. However, borrowers who need to cover large expenses or want predictable payments may find this option less practical.

–>Learn more about lines of credit in our guide How does a reverse mortgage line of credit work?

Option 4: Payout combinations

Using the combined payout option can offer both flexibility and predictability. Generally, borrowers can combine options in these ways:

- Modified term payouts combined with a line of credit: Borrowers can combine monthly payouts for a fixed period and access a credit line later. Monthly payouts could address current needs, and the line of credit could be used for emergencies later.

- Modified tenure payouts combined with a line of credit: As long as borrowers live in the home, they can receive modified tenure payouts. Under this plan, a borrower will receive smaller amounts but can access a line of credit anytime. Even if a borrower exhausts their line of credit, the monthly payouts will continue.

In tenure-based or modified tenure plans, payouts continue so long as the borrower lives in the home as their principal residence, pays all property taxes and insurance, maintains the home, and complies with all other loan terms. With modified tenure plans, the lender will set aside a specific amount of money for a line of credit.

The primary advantage of combining payout options is flexibility. By pairing monthly payouts with a line of credit or partial lump sum, borrowers could address immediate cash needs while keeping additional funds available for future or unexpected expenses.

Can you change the way you receive your loan proceeds?

Yes, it is possible to change the way you want to receive your proceeds. However, it is generally only possible at certain times.

- Before closing: If borrowers decide to receive monthly payouts instead of a lump sum, they can change their minds before closing.

- After closing: A borrower can change how they want to receive proceeds if they pick a payout option other than a lump sum at a fixed rate. The servicer can assist in making the change to the borrower’s payout method. Changing proceeds post-closing may require a servicing charge.

- Refinancing: If you refinance your reverse mortgage, you will likely have the option to change how you receive proceeds. However, refinancing comes with its own costs and can increase your overall loan balance.

Which reverse mortgage payout option is best?

There isn’t a single payout option that works best for everyone. The right choice depends on how you plan to use your home equity, your current cashflow needs, and how you want to prepare for future expenses. This chart breaks down the core advantages and considerations, but we’ll explore when each option may be the right choice in more detail below.

| Payout option | Best for | Key advantages | Important considerations |

| Lump sum | Immediate, large expenses | One-time access to a larger amount of cash at closing | Higher initial loan balance; less flexibility later |

| Line of credit | Flexible, future needs | Funds available as needed; interest only on amounts used | No built-in monthly payouts |

| Monthly payouts | Ongoing cash flow | Predictable payments over time | Less flexible for large expenses |

| Payout combinations | Short- and long-term planning | Blends cash flow, flexibility, and access to funds | Requires more upfront planning |

When to choose a lump sum payout

A lump sum payout may make sense for borrowers who need access to a larger amount of cash up front. This option is often used to pay off an existing mortgage (which is required for a HECM loan), eliminate higher-interest debt, or cover a significant one-time expense.

Because interest begins accruing the full amount right away, this option tends to result in a higher loan balance sooner. Borrowers who choose a lump sum typically have a clear, immediate use for the funds and are comfortable accessing a larger portion of their equity at closing.

It is worth noting that the lump sum option is available for some, but not all, reverse mortgages.

When to choose a line of credit

A line of credit may be a strong fit for borrowers who value flexibility and want access to funds over time rather than all at once. This option allows equity to remain available for future needs, whether that’s covering unexpected expenses, supplementing cash flow later in retirement, or providing a financial buffer.

Since interest accrues only on the amount drawn, a line of credit could help manage borrowing more gradually. This approach often appeals to borrowers who do not need additional cash right away but want to know they can access the funds when needed.

When to choose a monthly payout

Monthly payouts may be a good fit for borrowers looking to supplement cashflow on an on-going basis. These payments could help cover everyday living expenses, healthcare costs, or other recurring obligations.

Term payouts may work for those who want higher payouts over a set period, while tenure payouts are designed to last as long as the borrower lives in the home as their principal residence and meets all loan obligations. This option may provide consistency and predictability, though it may be less flexible for handling large, unexpected expenses without combining it with another payout method.

When to choose a combination

A combination payout may make sense for borrowers who want to address current financial needs while maintaining a bit of flexibility for the future. This approach allows borrowers to receive proceeds now—through monthly payouts—while preserving additional funds in a line of credit or accessing a smaller lump sum for planned expenses.

Combination options are often a good fit for borrowers with evolving financial goals, such as those planning for healthcare costs, home repairs, or future lifestyle changes. By spreading access to equity over time, this strategy could help balance cash flow needs while avoiding drawing more funds than necessary upfront.

How much could you be eligible for with a reverse mortgage loan?

How much you could be eligible to receive with a reverse mortgage depends on several factors, including your age, the value of your home, current interest rates, and the type of reverse mortgage you choose. FHA guidelines—like the 60% utilization rule for HECMs—also shape how much equity may be available upfront and how the rest can be accessed over time.

Wondering how much you might be eligible for with a reverse mortgage? Find out with our reverse mortgage calculator.

Frequently asked questions

When does a reverse mortgage have to be repaid?

A reverse mortgage typically becomes due when the borrower no longer lives in the home as their principal residence. This may happen if the home is sold, the borrower moves out permanently, or the last borrower passes away. The loan may also become due if loan obligations—such as paying property taxes and insurance or maintaining the home—are not met.

Can you take a lump sum from a reverse mortgage?

Yes, borrowers may take a lump sum from a reverse mortgage, depending on the loan type. Fixed-rate HECM loans require borrowers to take a lump sum at closing, while adjustable-rate HECM loans may offer a lump sum combined with other payout options. FHA rules, including the 60% utilization guideline, limit how much may be accessed upfront.

What are the payment options for a reverse mortgage?

Reverse mortgage payment options include a lump sum payout, monthly payments, a line of credit, or a combination of these options. Monthly payments may be structured as term payments for a set period or tenure payments designed to last for life, as long as the borrower meets all loan requirements.

What is the FHA lending limit for a reverse mortgage loan?

The FHA lending limit for a home equity conversion mortgage (HECM) in 2026 is $1,249,125. This limit caps the maximum home value used to calculate available loan proceeds, regardless of how much the home is worth or how much equity the borrower has.

About the author

is the Web Content Manager at Finance of America and a journalist with more than 10 years of experience whose work has appeared in MoneyWise, MSN, Yahoo! Finance, and The Motley Fool. She specializes in making complex financial topics accessible and is passionate about advancing financial literacy.

Disclaimer

This article is intended for general informational and educational purposes only and should not be construed as financial or tax advice. For tax advice, please consult a tax professional. For more information about whether a reverse mortgage fits into your retirement strategy, you should consult your financial advisor.