Explore by category

What is a reverse mortgage and how does it work?

In this article:

- What is a reverse mortgage?

- How do reverse mortgages work?

- What are the three types of reverse mortgage?

- Who might be eligible for a reverse mortgage?

- How are reverse mortgage proceeds paid out?

- How are reverse mortgage costs and fees structured?

- What are the benefits of a reverse mortgage?

- What are the risks of a reverse mortgage?

- How does a reverse mortgage compare vs other home equity options?

- What happens at the end of a reverse mortgage?

- Is a reverse mortgage right for me?

- Getting a reverse mortgage: Next steps

- Frequently asked questions about reverse mortgages

Key Takeaways

A reverse mortgage is a home loan for older homeowners that may convert part of their home’s equity into cash while continuing to live in the home. The loan is typically repaid when the home is sold, the borrower moves out, the last borrower passes away, or the loan terms are no longer met.

The most common type of reverse mortgage is a home equity conversion mortgage (HECM), which is insured by the Federal Housing Administration (FHA) and requires mandatory counseling to ensure borrowers understand the terms of the loan.

When the loan becomes due, borrowers or heirs have multiple options to resolve it, including selling the home, keeping it by repaying the balance, or transferring the property to the lender.

If you’re approaching or living in retirement, your home equity might be your biggest asset. But accessing that equity might feel like a big step, especially if it’s not something you’ve done before.

A reverse mortgage could allow you to tap into your home equity, but it comes with unique rules, costs, and long-term considerations. While you may have heard mixed opinions, understanding how these loans work could help you make the right decision. Reverse mortgages have been around for more than 60 years and are a highly regulated industry, with federal rules designed to help safeguard borrowers, eligible spouses, and their heirs.

This guide explains how reverse mortgages work, who may be eligible, the different loan types, payout options, what happens when the loan becomes due, and other key considerations. By the end, you’ll have a clearer understanding of whether a reverse mortgage may fit into your retirement and estate planning goals.

What is a reverse mortgage?

A reverse mortgage is a type of loan for older homeowners that may allow them to borrow money against the equity in their home. Unlike a traditional mortgage, a reverse mortgage does not require monthly mortgage payments.

Instead, funds are disbursed to the homeowner, and the loan balance increases over time as interest and fees are added. Borrowers must live in the property as their primary residence, maintain the home, and continue to pay property taxes, homeowners association fees, and insurance costs to keep the loan in good standing. Failure to meet the loan terms will result in the loan becoming due.

The loan is typically repaid by selling the home, though you or your heirs may choose to pay out of pocket or get a traditional mortgage to resolve the balance. The age requirements vary by loan type: typically 62 or older for FHA-insured home equity conversion mortgages (HECMs) and 55 or older for some proprietary reverse mortgages.

How do reverse mortgages work?

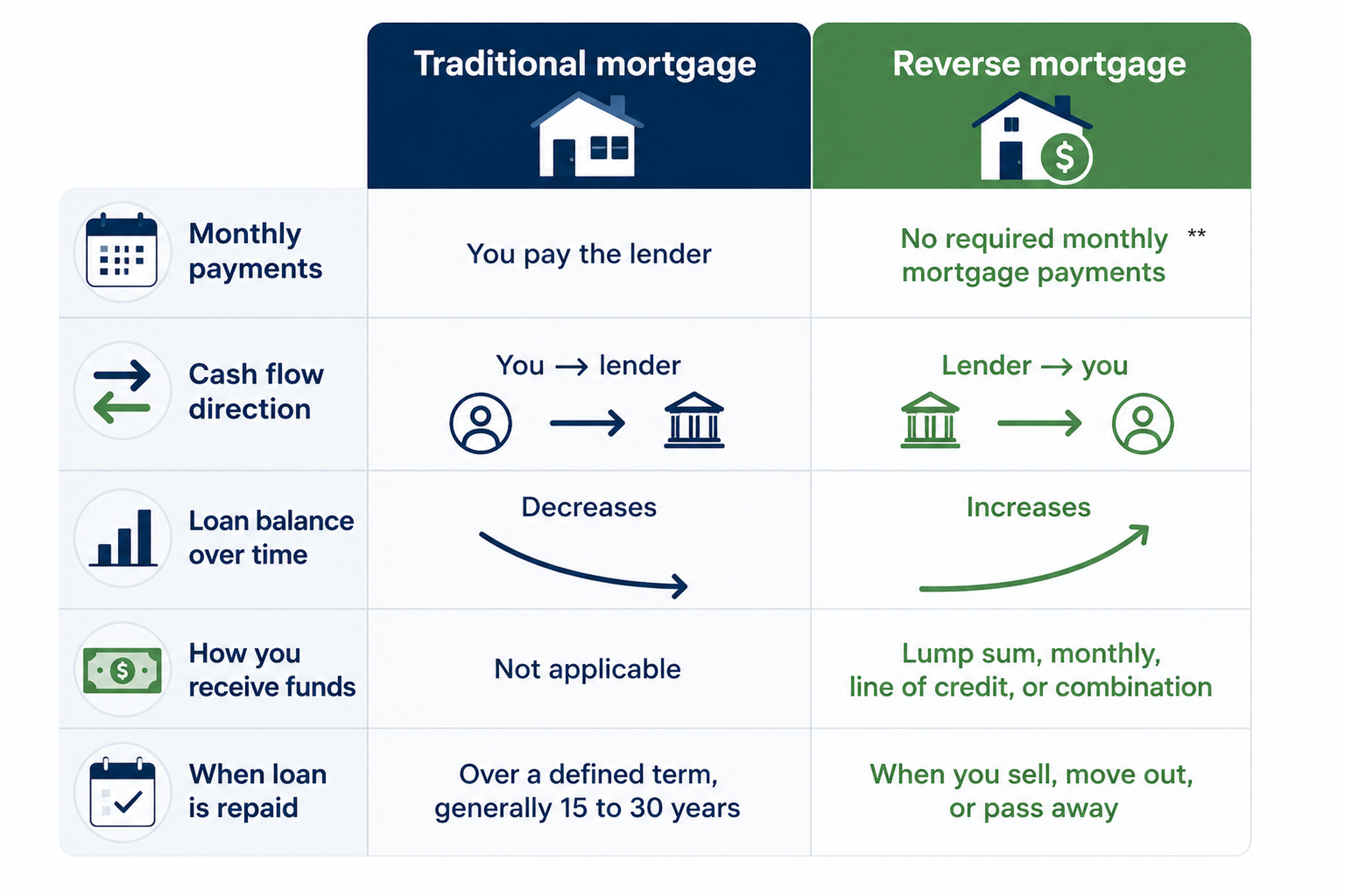

The simplest way to understand a reverse mortgage is to compare it to something you’re already familiar with: a traditional mortgage. In a traditional, or forward, mortgage, you borrow money from a lender to buy a home, then make monthly payments over time to pay down the balance.

With a reverse mortgage, instead of making payments to a lender, you receive loan payouts based on the equity in your home. You continue to live in your home, and interest and fees are charged each month, which increases the loan balance and decreases your home equity over time.

Loan repayment is typically deferred until:

- The last surviving borrower or eligible non-borrowing spouse dies; or

- The last surviving borrower or eligible non-borrowing spouse moves out of the home; or

- The borrower cannot meet other loan terms (such as maintaining the home or paying insurance, property taxes, and other fees).

In short, a reverse mortgage loan stays deferred as long as the borrower remains in the home and meets all loan obligations.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

A reverse mortgage example

Let’s say Joseph is a 70-year-old widower who owns his home outright. After the death of his wife, he’s looking for a way to access some of his home’s equity to fund a few trips and cover some medical expenses.

Because Joseph is over 62 and lives in the home as his primary residence, he decides to explore a reverse mortgage. After researching, completing the required counseling, and applying with a lender, his house is appraised to determine how much equity may be available based on his age, interest rates, and the home’s value.

Joseph chooses ongoing monthly payments from loan proceeds for more financial flexibility, but reverse mortgage funds can also be received as a lump sum, line of credit, or a combination of options. He uses the monthly cash flow to cover medical costs and takes a few trips to see his adult daughter.

A few years later, Joseph decides to sell the home and move closer to his daughter and her family. At that point, the loan becomes due, so he uses the sale proceeds to repay his reverse mortgage. Any remaining equity belongs to Joseph.

What are the three types of reverse mortgage?

TThe most popular type of reverse mortgage is HECM loans, which are insured by the Federal Housing Administration (FHA) and must meet specific requirements from the U.S. Department of Housing and Urban Development (HUD).

There are also proprietary reverse mortgages, where the lender sets their own terms, and single-purpose reverse mortgages, which are often supported by local governments or public agencies for specific uses. These alternatives to HECMs may be suitable for borrowers with higher home values or specific needs.

Here’s how they differ:

| Feature | HECM (FHA-insured) | Proprietary reverse mortgage | Single-purpose reverse mortgage |

| Who offers it | FHA-approved lenders | Private lenders | State/local agencies or nonprofits (including local governments) |

| Minimum age | 62+ | Varies by lender (sometimes 55+) | Usually 62+ |

| FHA insured | Yes | No | No |

| Non-recourse protection | Yes (required)1 | Varies by lender | Varies |

| Maximum loan amount | Subject to FHA lending limits ($1,249,125 in 2026) | Often higher than HECM limits | Usually low; intended to cover specific costs |

| Payout options | Lump sum, monthly payments, line of credit, or combination | Varies by lender | Approved purpose only |

| Use of funds | Flexible (living expenses, medical costs, mortgage payoff, etc.) | Generally flexible | Restricted (Often for real estate taxes, insurance, repairs) |

| Required counseling | Yes (HUD-approved) | Often required | Often required |

| Availability | Nationwide | Limited by lender and state | Limited by location; not offered by all local governments or for all purposes. |

Home equity conversion mortgages (HECMs)

A HECM loan is insured by the FHA and is specifically designed for homeowners 62 and older seeking to access their home equity. HECMs are the most widely used type of reverse mortgages and are available through FHA-approved lenders..

HECM reverse mortgages offer regulatory safeguards, including mandatory HUD-approved counseling to ensure borrowers understand the costs, financial implications, alternatives, as well as the non-recourse protection1. This means borrowers or their heirs will never owe more than the home’s value when the loan becomes due, even if the loan balance exceeds the home’s market value at the time of sale. The lending limit is set by HUD and is $1,249,125 in 2026.

Costs for a HECM reverse mortgage may include an upfront mortgage insurance premium of 2% of the home’s appraised value, along with an annual fee of 0.5% of the outstanding loan balance. Interest is also charged on the total loan balance. Borrowers should understand all associated reverse mortgage costs before proceeding.

HECMs provide multiple payout options, including a lump sum, monthly payments, a line of credit, or a combination of these options. Loan amounts are subject to FHA lending limits and are based on factors such as the borrower’s age, interest rates, and the home’s appraised value.

Proprietary reverse mortgages

Proprietary reverse mortgages are offered by private lenders and are not insured by the FHA. These loans may be an option for homeowners with higher-value homes that exceed FHA lending limits. Jumbo reverse mortgages, which allow access to higher loan amounts, are a common type of proprietary loan.

Because proprietary reverse mortgages are not FHA-insured, terms, costs, and consumer safeguards vary by lender. Some proprietary loans offer non-recourse protections1 similar to HECMs, while others may not. For this reason, reviewing loan terms carefully is especially important. Proprietary loans may be available to borrowers younger than 62 in certain states, though eligibility requirements and minimum age limits vary.

→Learn more about HomeSafe, a proprietary reverse mortgage from Finance of America designed for higher-value homes.

The HomeSafe reverse mortgage is a proprietary product of Finance of America and is not related to the Home Equity Conversion Mortgage (HECM) program. HomeSafe products are only available in certain states. Please contact us for a complete list of availability.

Single-purpose reverse mortgages

Single-purpose reverse mortgages are typically offered by state or local government agencies or nonprofit organizations. These loans are designed for specific, approved uses, such as paying real estate taxes, flood insurance premiums, homeowners insurance, or the cost of essential home repairs.

Because the funds are restricted to a specific use, single-purpose reverse mortgages are usually less flexible than HECMs or proprietary loans. Availability can vary by location, and not all homeowners will be eligible.

Considering a reverse mortgage? To learn more, visit the CFPB’s Reverse Mortgage: A Discussion Guide.

Who might be eligible for a reverse mortgage?

Reverse mortgage eligibility is based on several factors, including age, homeownership status, residency, and financial responsibilities. While specific requirements vary by loan type and lender, most loans have similar qualifications.

General eligibility requirements include:

| Requirement | What it means |

| Age | 62+ for HECM; 55+ for some proprietary loans |

| Home ownership | Own the home outright or have low remaining mortgage balance |

| Residency | Live in the home as your primary residence |

| Property type | Single-family, FHA-approved condos or manufactured homes, certain multi-unit buildings |

| Counseling | Meet with a HUD-approved counselor; required for all HECM reverse mortgages and most proprietary reverse mortgages |

| Financial assessment | Lenders review your assets, income, and financial history to ensure you can meet the loan terms. Having delinquent federal debt may disqualify you |

To keep the loan in good standing, you must meet and continue to meet all the loan terms, including maintaining primary residency, maintaining the home, and paying property taxes, insurance costs, and homeowners association fees.

→For more information about eligibility rules and how they apply to different situations, read our full guide on reverse mortgage eligibility requirements.

How are reverse mortgage proceeds paid out?

The disbursement options available for a reverse mortgage depend on the type of reverse mortgage and the lender. Common reverse mortgage proceed options include:

- Lump sum: Receive most of the loan proceeds at closing

- Monthly payments: Receive monthly payouts

- Line of credit: Access funds as needed over time

- Combination options: A mix of the other three options

The type of reverse mortgage you choose may affect which distribution options are available. For example, HECM loans typically offer the most flexibility, while proprietary and single-purpose reverse mortgages may limit how and when funds are disbursed.

How are reverse mortgage funds generally used?

Reverse mortgage proceeds are flexible and can be used for a variety of expenses. Most borrowers use the funds from their reverse mortgage to:

- Pay off an existing mortgage (required for HECMs)

- Tackle higher-interest debt

- Cover everyday living expenses

- Pay for medical costs

- Fund home repairs, accessibility upgrades, or maintenance

- Build a financial buffer for unexpected expenses

Because how you receive and use the funds can affect loan growth and long-term outcomes, choosing the right payment structure is an important part of the decision-making process. Learn more about your options in our guide to payout options.

How are reverse mortgage costs and fees structured?

Reverse mortgages come with both upfront and ongoing costs. Different reverse mortgage products may have different costs and fees, so make sure to compare your options and work with a reputable lender.

Here’s what to expect:

- Origination fees: Fees charged by the lender to process the loan. For HECM loans, these fees are capped by FHA guidelines.

- Closing costs: May include appraisal fees, title insurance, recording fees, and other third-party charges.

- Counseling costs: HECM loans and some proprietary reverse mortgages require borrowers to attend and pay out of pocket for a HUD-approved counseling session.

- Mortgage insurance premiums (MIP): Required for HECM loans and paid to the FHA.

- Interest charges: Interest accrues on the loan balance over time, increasing the amount owed.

- Servicing fees: Some reverse mortgage companies charge monthly fees for managing the loan, though this varies by lender and loan type.

- Ongoing costs: Borrowers must continue to pay property taxes, homeowners insurance, and maintain the home. Failure to pay these recurring costs can result in default and potential foreclosure.

The total cost of a reverse mortgage depends on factors such as the loan type, interest rate, home value, and how long the loan remains outstanding. While some costs may be financed as part of the loan, this increases the amount owed and can affect how much equity remains in the home over time.

→To learn more, read our full guide on reverse mortgage costs and fees.

What are the benefits of a reverse mortgage?

Just like any financial product or loan, reverse mortgages aren’t right for every person or every situation. There are potential advantages for some borrowers, but also risks that need to be considered. Advantages include:

- Access your home equity: Reverse mortgages allow eligible homeowners to convert home equity into cash while continuing to live in their home, as long as they meet the terms of the loan.

- No required monthly mortgage payments: As long as you live in the home as your primary residence, maintain the home, and pay property taxes, fees, and insurance costs, you do not have to make payments on the loan.

- Tax-free loan proceeds: Funds received from a reverse mortgage are loan proceeds, not income, and generally are not subject to federal income tax. This is not tax advice— talk to a tax professional for more information.

- Non-recourse protection (HECM loans)1: For FHA-insured HECM loans, borrowers and heirs will never owe more than the home’s value when the loan becomes due.

- Improved financial flexibility in retirement: Reverse mortgages may help cover living expenses, healthcare costs, or provide a financial buffer for unexpected costs.

- Borrower safeguards: Mandatory counseling and federal regulations help ensure borrowers understand the loan’s terms, costs, and responsibilities.

What are the risks of a reverse mortgage?

Like any loan, there are risks to taking out a reverse mortgage. Understanding these drawbacks is an important part of making an informed decision.

- Loan balance increases over time: As interest and fees accrue, the outstanding loan balance grows, reducing the amount of equity that may remain for your heirs.

- Upfront costs may be higher: Reverse mortgages often carry higher upfront fees than some traditional home equity options.

- Ongoing homeowner responsibilities: Borrowers must continue paying property taxes and homeowners insurance, maintain the home, and live in the property as their primary residence.

- Loan may become due if terms aren’t met: Moving out permanently, entering long-term care, or failing to meet loan obligations may cause the loan to become due.

- Complex loan structure: Reverse mortgages involve long-term financial and estate planning considerations that may not be suitable for every homeowner.

How does a reverse mortgage compare vs other home equity options?

Your home’s equity can be a powerful financial tool, but reverse mortgages aren’t the only way to access it. In some cases, refinancing, a home equity loan, home equity line of credit (HELOC), or downsizing might be a better fit.

- Cash-out refinance: You replace your current mortgage with a new one—potentially with a different rate or term—and take out a portion of your home equity as cash. This increases your loan balance and may result in a higher monthly payment.

- Home equity loan: Provides a one-time lump sum that is repaid through fixed monthly payments over a set period, typically 5 to 15 years. It may offer predictable payments and lower upfront costs, but requires steady income and adds a new monthly obligation.

Finance of America does not currently offer home equity loans. - HELOC: Offers flexible access to funds through a revolving line of credit, often with variable interest rates. Borrowers may make interest-only payments during the initial draw period, followed by full repayment later. Requires income and credit history qualification, and introduces ongoing payment responsibilities.

- Downsizing to a smaller home: Involves selling your current home and purchasing a smaller, less expensive property. This option may work well for those open to moving, but often comes with trade-offs, such as relocation, expenses, and leaving a familiar environment.

This chart breaks down the core differences between the different home equity options:

| Feature | Reverse mortgage | Cash-out refinance | Home equity loan | HELOC | Downsizing |

| Minimum age | 62+ (HECM) | 18+ | 18+ | 18+ | 18+ |

| Monthly mortgage payments | Not required* | Required | Required | Required | Only if you finance a new home |

| Access to cash | Lump sum, monthly payments, line of credit, or combination | Lump sum; Difference between current home value and exisiting mortgage balance | Lump sum payment | Line of credit | From sale proceeds |

| Income required for eligibility | Limited (a financial assessment is required) | Yes | Yes | Yes | Only if you finance a new home |

| Interest rate type | Fixed or adjustable | Fixed or adjustable | Fixed or adjustable | Generally variable; some lenders may offer fixed rates | Depends on if you finance a new home |

| Loan repayment timing | When home is sold, borrower moves out, passes away, or fails to meet loan terms | Over loan term | Over loan term | Over draw + repayment period | None; unless you take out a new mortgage |

| Impact on home equity | Decreases over time | Increases gradually | Increases with payments | Decreases if balance grows/increases as the loan is repaid | Equity converted to cash |

| Ability to stay in current home | Yes** | Yes | Yes | Yes | No |

| Negative amortization? | Yes, interest accrues over time and is added to loan balance | No, loan balance decreases as you pay down the loan | No, loan balance decreases with principal and interest payments | No, starts as interest only during draw period, then converts to fully amortizing loan during repayment period | Not a loan (unless you buy again) |

| Good choice for: | Retirees seeking cash flow without monthly payments* | Borrowers wanting lower rates or who plan to stay in the home a long time | Borrowers who can manage fixed payments | Flexible short-term needs | Homeowners ready to relocate |

*The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

**The right to remain in the home is contingent on paying property taxes and homeowner’s insurance, maintaining the home, and complying with the loan terms

What happens at the end of a reverse mortgage?

A reverse mortgage becomes due when specific events occur. Understanding these triggers ahead of time may help borrowers and their families prepare for repayment and avoid surprises.

The loan typically comes due when:

- The borrower sells the house

- The borrower no longer lives in the home as a primary residence

- The last surviving borrower or eligible nonborrowing spouse dies

- The borrower fails to maintain the home or pay property taxes

- The borrower otherwise violates the terms of the loan

When any of these events occur, you or your heirs have four main options:

1. Sell the home

The borrower or heirs can choose to sell the home, then use the proceeds from the sale of the house to pay the loan balance.

→Learn more: Are heirs responsible for reverse mortgage debt?

2. Keep the home

Borrowers or their heirs may keep the home by paying off the reverse mortgage balance or 95% of the home’s appraised value, whichever is less (for HECM loans). Borrowers may use cash or refinance into a new mortgage.

In some cases, if an heir is age 62 or older, a new reverse mortgage may be an option. Certain proprietary reverse mortgages may be available to heirs as young as 55, depending on the state and lender.

3. Sign over the title and complete a deed in lieu of foreclosure

The heirs can give the property to the lender by signing a deed in lieu of foreclosure. This act satisfies the debt and will prevent foreclosure of the house. However, this forfeits any remaining equity.

4. Do nothing

If the borrower or their heir chooses to do nothing with the loan, the lender will foreclose on the home. Allowing the loan to go to foreclosure forfeits any remaining equity and should be avoided. Heirs should work with the lender to resolve the loan before foreclosure proceedings begin.

Is a reverse mortgage right for me?

A reverse mortgage isn’t the right choice for everyone or at every stage of life. It may be a better fit for some homeowners than others, depending on their financial goals, lifestyle, and long-term plans.

A reverse mortgage may be worth considering if you:

- Want to access your home equity without taking on required monthly mortgage payments

- Plan to stay in your home long-term

- Have significant equity built up in your home

- Are looking to create more flexible cash flow

- Prefer to remain in your home rather than downsize or relocate

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

It may be less suitable if you:

- Plan to move in the near future

- Want to preserve as much home equity as possible for your heirs

- Are comfortable managing monthly payments through other loan options

- Do not meet ongoing loan obligations, such as property taxes, insurance, and home maintenance

If you think a reverse mortgage isn’t a good fit, other home equity options like a second reverse mortgage or HELOC may be worth considering. They have different eligibility rules and may work better with your financial goals.

Getting a reverse mortgage: Next steps

A reverse mortgage may help eligible homeowners access home equity while continuing to live in their home, but it isn’t the right solution for everyone. Understanding how the loan works, the costs involved, and the long-term responsibilities is essential.

If you’re exploring reverse mortgages, consider your future plans, discuss options with family members, and speak with a HUD-approved housing counselor. You can also use our reverse mortgage calculator to estimate how much equity may be available to you.

Frequently asked questions about reverse mortgages

Can I lose my home with a reverse mortgage?

Yes, you may lose your home if you fail to meet the loan’s requirements. However, it is not an automatic or fast process. As long as you continue to pay property taxes and homeowners insurance, maintain the home, and live in it as your primary residence, you may remain in your home for as long as you choose.

If a required obligation is missed, the lender must follow a formal process that includes required notices and opportunities to correct the issue before foreclosure may occur.

What happens if I outlive the equity from my reverse mortgage?

You cannot outlive a reverse mortgage or be required to leave your home because the loan balance grows larger than the home’s value. FHA-insured HECM loans are non-recourse, meaning you may continue living in the home as long as you meet the loan’s requirements, even if the balance exceeds the home’s market value. 1

Can I still leave my home to my kids with a reverse mortgage?

Yes, you may lose your home if you fail to meet the loan’s requirements. However, it is not an automatic or fast process. As long as you continue to pay property taxes and homeowners insurance, maintain the home, and live in it as your primary residence, you may remain in your home for as long as you choose.

What happens if I outlive the equity from my reverse mortgage?

You cannot outlive a reverse mortgage or be required to leave your home because the loan balance grows larger than the home’s value. FHA-insured HECM loans are non-recourse1, meaning you may continue living in the home as long as you meet the loan’s requirements, even if the balance exceeds the home’s market value.

Can I still leave my home to my kids with a reverse mortgage?

Yes, you may leave your home to your children even with a reverse mortgage. However, when you die, the loan becomes due, and your children must choose how to resolve it. They may pay off the reverse mortgage loan balance either with their own funds, by selling the home, or taking out a traditional mortgage.

How does a reverse mortgage impact government benefits like Medicare and Social Security?

A reverse mortgage does not affect Medicare or Social Security benefits. Funds received from a reverse mortgage are loan proceeds, not income, and therefore do not count toward these programs. However, it may affect eligibility for needs-based programs such as Medicaid or Supplemental Security Income (SSI), which have asset limits.

How does a reverse mortgage work when you die?

If your spouse survives you and is either a co-borrower or eligible non-borrowing spouse, they may remain in the home as long as the terms of the loan are met, including maintaining the home, living in it as their primary residence, and paying taxes, fees, and insurance. When the last borrower or eligible non-borrowing spouse dies, the loan becomes due. Your heirs may pay off the loan and keep the home, or sell the home, repay the loan, and keep the remaining equity.

Are reverse mortgages government-insured?

Home equity conversion mortgages (HECMs) are insured by the FHA. This insurance provides important borrower safeguards, including non-recourse coverage1 and safeguards for borrowers and eligible spouses. Other types of reverse mortgages, such as proprietary or single-purpose reverse mortgages, are not FHA-insured and may have different terms, costs, and protections.

Are reverse mortgages a scam?

No, they are a valid financial tool for older homeowners. However, scammers use many different tactics to take advantage of people, so make sure to work with a trusted lender and be wary of high-pressure tactics.

1 Non-recourse means that you, or your estate, can’t owe more than the value of your home when the loan becomes due and the home is sold. Non-recourse means that if you default on the loan, or if the loan cannot otherwise be repaid, the lender cannot look to your other assets (or your estate’s assets) to meet the outstanding balance on your loan.

About the author

is the Web Content Manager at Finance of America and a journalist with more than 10 years of experience whose work has appeared in MoneyWise, MSN, Yahoo! Finance, and The Motley Fool. She specializes in making complex financial topics accessible and is passionate about advancing financial literacy.

Disclaimer

This article is intended for general informational and educational purposes only and should not be construed as financial or tax advice. For tax advice, please consult a tax professional. For more information about whether a reverse mortgage fits into your retirement strategy, you should consult your financial advisor.