Explore by category

Traditional vs. reverse mortgage: What’s the difference?

In this article:

Key Points

The key difference between a reverse mortgage and traditional mortgage is how funds flow.

In a traditional mortgage, you borrow money and make payments to reduce the loan balance over time.

With a reverse mortgage, you borrow money and the loan proceeds are sent to you. The loan balance increases over time, and is often repaid using proceeds from selling the home, though there are other options.

Quick Answer: Traditional mortgages require monthly mortgage payments that reduce the loan balance over time, while a reverse mortgage may allow eligible homeowners to convert home equity into cash with no required monthly mortgage payments as long as borrowers live in the home most of the year, maintain the home, and pay property taxes, insurance, and fees.

While most people have a decent grasp of what a traditional mortgage is (often called a forward mortgage), fewer understand what a reverse mortgage is and how it works. Understanding the differences is important, especially if you’re considering a reverse mortgage.

The reality is these are very different financial products, so it’s a bit like comparing a bicycle to a rowboat— yes, they’re both modes of transportation, but the mechanics are quite different.

Key differences between a traditional mortgage and a reverse mortgage

The main difference between a traditional forward mortgage and a reverse mortgage is the way the money flows. With a traditional mortgage, you borrow money, make payments, and the loan balance decreases as you pay it off.

With a reverse mortgage, you borrow money, don’t make monthly mortgage payments, and the loan balance increases over time. During the life of the loan, you must continue living in the property as a primary residence, maintain the home, and pay all property costs, including taxes, fees, insurance, and homeowners’ association fees.

When you no longer meet those requirements, the loan becomes due. Most people pay off the reverse mortgage with the proceeds from selling the home, but you can also pay it off with your own funds, or your heirs can take out a traditional mortgage to satisfy the loan.

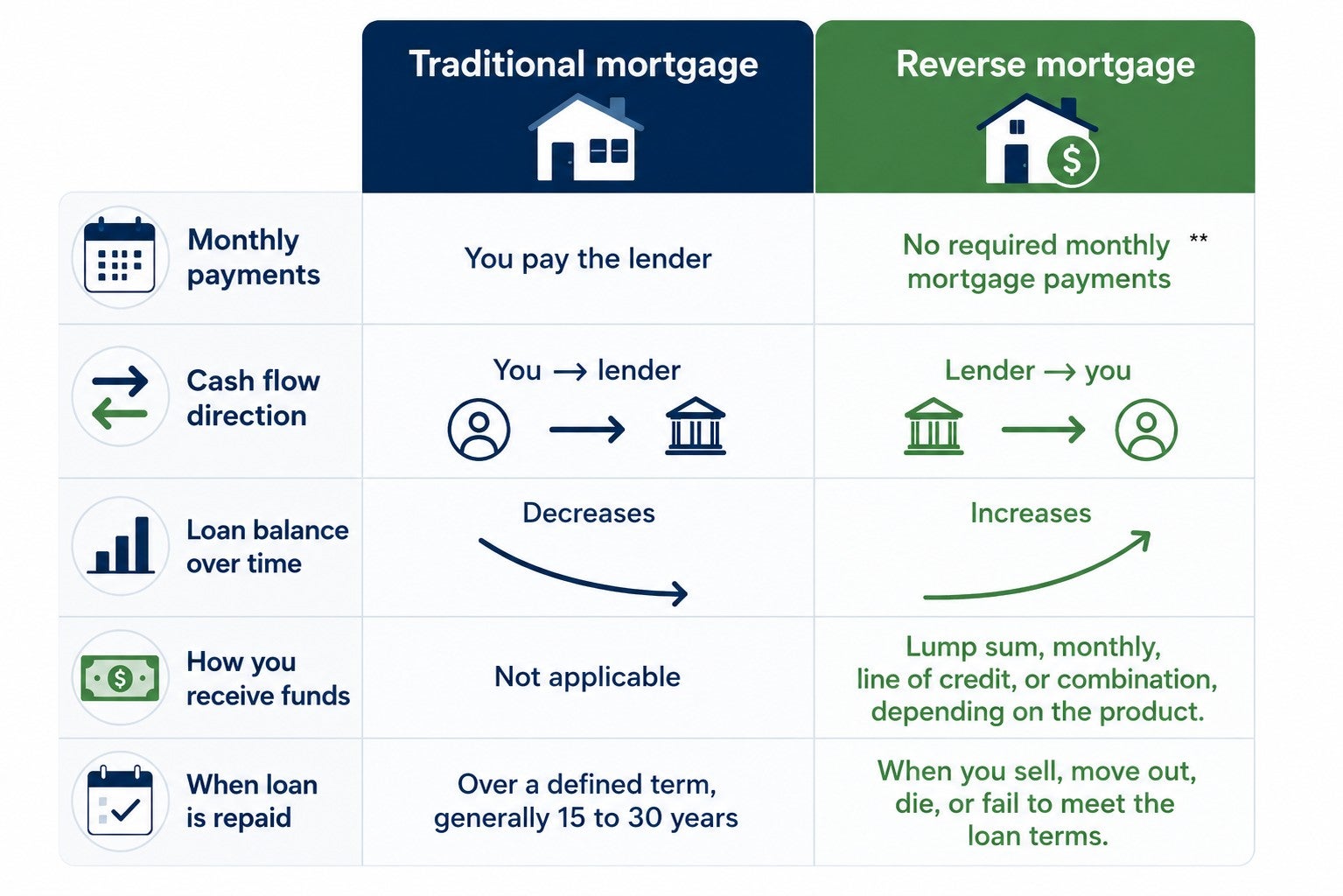

This chart breaks down the core differences between a traditional mortgage and a reverse mortgage.

| Traditional mortgage | Reverse mortgage | |

| Age requirement | Applicants must be of legal age to sign the contract. | Borrowers must be 62 or older for a Home Equity Conversion Mortgage (HECM), the most common type of reverse mortgage.* |

| Credit score requirement | Determined by the lender. | No minimum credit score is required for a HECM. |

| Financial obligations | Required monthly mortgage payments. | Must pay property taxes, fees, HOA dues, insurance, and maintain the property. |

| Loan term | Varies; often 10, 20, or 30 years. | No fixed term. |

| Interest rate | Fixed or adjustable rates are available. | Fixed interest rate only available for lump sum option; other payment disbursements available with an adjustable rate. |

| Interest payment | The borrower pays interest monthly. As payments are made over time, less money will be applied toward interest. | Interest is charged to the balance monthly, but not due until the end of the loan. The total loan balance grows over time. |

| Monthly payment | Monthly mortgage payments are required, including interest and principal. | No monthly mortgage payments are required.** |

| Loan disbursement | Most traditional mortgages don’t have any disbursement. In the case of a cash-out refinance, disbursement is a single lump sum payment. | Borrowers can receive disbursements as a lump sum, monthly payout, line of credit, or some combination of these options. (Available options can vary by product.) |

| Counseling requirement | No counseling is required. | Third-party counseling is required with a HUD-approved counselor. |

| Loan maintenance | If monthly payments are made to the lender, the borrower is current with the loan. | The borrower must live in the home; maintain the home; and pay applicable property taxes, insurance, and homeownership dues. |

*Some proprietary reverse mortgage products may have lower age requirements.

**The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

To learn more, please visit the CFPB’s “Reverse Mortgage: A Discussion Guide.”

How do reverse mortgages work?

Reverse mortgages may allow older homeowners (typically age 62+) to convert a portion of their home equity into cash without being required to make monthly mortgage payments. Instead of paying down a loan balance over time, the balance gradually increases as funds are withdrawn and interest accrues, which reduces the remaining equity in the home.

These loans are generally a better fit for those planning to stay in their homes long-term. Home Equity Conversion Mortgage (HECMs), the most common type of reverse mortgage, are federally regulated with safeguards designed to help protect homeowners from predatory lending.

While no monthly mortgage payments are required, borrowers must live in the home as their primary residence and are still responsible for property taxes, homeowners insurance, and basic home maintenance. The loan becomes due when the borrower moves out, sells the home, passes away, or otherwise fails to meet the loan terms.

There are three main types of reverse mortgages:

- HECM: This type of loan is federally insured and regulated. It may be available to homeowners aged 62+ and features flexible payout options and built-in consumer safeguards.

- Proprietary reverse mortgages: These are private loans offered by lenders and not backed by the federal government. These are often designed for higher-value homes and may allow access to more equity. Some products may be available to homeowners as young as 55 in some states.

- Single-purpose reverse mortgages: Typically offered by state or local agencies or nonprofits. Funds generally must be used for a specific purpose, like home repairs or property taxes, and are not available everywhere.

If you’re considering buying a home with a reverse mortgage, it may be worth considering a HECM for purchase. This loan may allow homeowners 62+ to buy a new primary residence using a reverse mortgage in combination with a down payment.

What are the costs associated with a reverse mortgage loan?

Like any mortgage, a reverse mortgage comes with upfront and ongoing costs. The structure may feel a bit different, but most fees are similar to what you’d see with a traditional loan—just handled differently.

- Counseling costs: For HECMs, borrowers must pay for and attend a counseling session with a HUD-approved counselor.

- Closing costs: Includes typical fees like appraisal, title, and origination.

- Mortgage insurance premium (MIP): Required for federally insured reverse mortgages to guarantee the loan payments continue and provide non-recourse protection.1

- Interest: Accrues over time and is added to the loan balance.

- Servicing fees: May be charged by the lender to manage the loan (not all loans include this).

- Property fees: You must continue to pay property taxes, maintenance costs, insurance, and other fees.

Some of these costs can be rolled into the loan, but they increase the total loan balance over time.

→ Learn more about the costs and fees associated with a reverse mortgage.

What are the eligibility requirements for a reverse mortgage?

Reverse mortgages have a few key eligibility requirements focused on age, home type, and financial responsibility. While exact criteria may vary slightly by loan type, most borrowers need to meet the following:

| Requirement | What it means |

| Age | At least 62 years old (for HECMs), 55+ for some proprietary loans |

| Homeownership | Must own the home outright or have a low remaining mortgage balance |

| Primary residence | The home must be your primary residence |

| Eligible property | Typically, a single-family home, FHA-approved condo, or certain multi-unit properties. Some manufactured homes may be eligible |

| Financial assessment | Lenders review income, credit, and ability to keep up with taxes, insurance, and maintenance |

| Counseling | Required session with a HUD-approved counselor ( for HECMs) |

→ To learn more, read our article What are reverse mortgage eligibility requirements?

What are the risks of a reverse mortgage loan?

Reverse mortgages may be helpful in the right situation—but they aren’t risk-free. It’s important to understand the trade-offs before moving forward.

- Rising loan balance: As you borrow and interest accrues, your loan balance increases over time—reducing your home equity

- Higher overall costs: Fees, interest, and mortgage insurance may make this a more expensive option compared to alternatives like a home equity loan or HELOC

- Impact on heirs: Less remaining equity may be available to pass on to heirs

- Ongoing obligations: You must keep up with property taxes, insurance, and maintenance—or risk default

- Not ideal for short-term plans: If you move out sooner than expected, the loan becomes due, which may limit flexibility

Now that you understand the basics of a reverse mortgage, let’s talk about how a standard, forward mortgage works.

→ Are reverse mortgages good or bad? Learn more.

How do traditional mortgages work?

A forward mortgage is what most people think of as a traditional home loan. You borrow money to purchase or refinance a home and repay it over time through monthly payments. Typically, payments include both principal and interest, and your balance decreases as you pay down the loan—building equity in your home.

What are the costs for a traditional mortgage?

The exact cost for a traditional mortgage varies based on several factors, not the least of which is your interest rate. In general, you can expect to pay:

- Monthly mortgage payments: Typically include principal and interest

- Interest charges: The cost of borrowing, paid over the life of the loan

- Property taxes and insurance: Often included in monthly payments (if escrowed)

- Closing costs: Upfront fees like appraisal, origination, and title

What are the eligibility requirements for a traditional mortgage?

Lenders look at a combination of financial factors to determine eligibility:

| Requirement | What it means |

| Credit score | Helps determine loan approval and interest rate |

| Income and employment | Must show steady income to support monthly payments |

| Debt-to-income ratio (DTI) | Measures how much of your income goes toward debt |

| Down payment | Varies by loan type, but often required upfront |

| Property requirements | Home must meet lender and/or product standards |

What are the risks of a traditional mortgage?

Like most financial products, a forward mortgage comes with some risks. These include:

- Monthly payment obligation: Missing payments may lead to late fees or foreclosure

- Interest costs over time: You may pay significantly more than the purchase price over the life of the loan

- Market risk: Home values may decline, impacting your equity

- Upfront costs: Closing costs and down payment may be substantial

A forward mortgage is a long-term commitment, so it’s important to choose a loan that fits your budget and financial goals.

Reverse mortgage vs. Traditional mortgage example

Hopefully, you now have a better idea of how reverse mortgages and forward mortgages are different. Still, seeing a practical example can be helpful:

- Susan, 55, takes out a $400,000 forward mortgage to buy a home. Her bank pays the seller of the home, and she makes monthly mortgage payments to the bank. Eventually, she repays the loan in its entirety and the home lien is removed. Susan now owns her home outright.

- Robert, age 67, purchased a home 35 years ago and paid off the forward mortgage. After talking with a HUD-approved counselor to make sure he understands the terms of the loan, he applies for a HECM. He is approved and receives a lump sum payout, which he uses to pay for home upgrades.

Both are loans, but with a conventional mortgage, you use the borrowed funds to pay for a house, then pay it back. With a reverse mortgage, you may access home equity you’ve built and use those funds however you like. As long as you live in the home, maintain the property, and pay taxes, fees, and insurance, the reverse mortgage does not require monthly mortgage payments.

So, what happens when Susan and Robert decide to sell?

- A few years after paying off her conventional mortgage, Susan decides to sell her home. Since she owns it outright, all the equity is hers to keep. She uses those funds to buy a smaller condo in a beach town.

- After 10 years, Robert is ready to downsize. He sells his home and uses the proceeds to pay off his reverse mortgage. The remaining equity is his to keep, and he uses it to buy an RV so he can travel the country.

Is a reverse mortgage or traditional mortgage right for me?

Choosing between a forward and reverse mortgage comes down to your financial goals, stage of life, and how long you plan to live in your home. A forward mortgage helps you build equity over time through regular payments, but it comes with ongoing monthly obligations, interest costs, and upfront expenses.

A reverse mortgage allows you to access existing equity without monthly mortgage payments—but increases your loan balance and reduces the equity you leave behind. Both options carry risks and advantages, so the right choice depends on your individual situation.

See how much cash you could get with a reverse mortgage from Finance of America.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

Frequently asked questions about forward and reverse mortgages

What is a forward mortgage?

A forward mortgage is a traditional home loan where you borrow money to buy or refinance a home and repay it over time with monthly payments. As you pay down the balance, your equity increases.

What are the different types of reverse mortgages?

The three main types are HECMs (federally insured), proprietary reverse mortgages (private loans), and single-purpose reverse mortgages (for specific uses like repairs or taxes).

What are the downsides of a reverse mortgage?

A reverse mortgage reduces home equity available to you and your heirs and may cost more than other home equity alternatives. You must still pay taxes, insurance, and maintain the home or risk default.

Can you use a reverse mortgage to buy a new home?

Yes, with a HECM for purchase, you may use a reverse mortgage to buy a new primary residence, combining a down payment with loan proceeds. Like most reverse mortgages, no monthly mortgage payments are required.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

Can I get a reverse mortgage if I have an existing mortgage?

Yes, but in most cases, the existing mortgage must be paid off, often using proceeds from the reverse mortgage. Second reverse mortgages do not have this requirement—they leave the first mortgage in place, which maintains your rate and original loan terms.

1. Non-recourse means that you, or your estate, can’t owe more than the value of your home when the loan becomes due and the home is sold. Non-recourse means that if you default on the loan, or if the loan cannot otherwise be repaid, the lender cannot look to your other assets (or your estate’s assets) to meet the outstanding balance on your loan.

About the author

is the Web Content Manager at Finance of America and a journalist with more than 10 years of experience whose work has appeared in MoneyWise, MSN, Yahoo! Finance, and The Motley Fool. She specializes in making complex financial topics accessible and is passionate about advancing financial literacy.

Disclaimer

This article is intended for general informational and educational purposes only and should not be construed as financial or tax advice. For tax advice, please consult a tax professional. For more information about whether a reverse mortgage fits into your retirement strategy, you should consult your financial advisor.