Explore by category

Reverse mortgage myths: 14 misconceptions debunked

In this article:

- Myth #1: Reverse mortgages are risky or shady

- Myth #3: You’ll still have monthly mortgage payments

- Myth #4: Most reverse mortgages end in foreclosure

- Myth #5: My heirs will inherit debt, and I won’t leave anything to my children

- Myth #6: You can’t move or sell your home

- Myth #7: You need perfect finances to be eligible for a reverse mortgage

- Myth #8: Reverse mortgages are only for people in financial distress or as a last resort

- Myth #9: Reverse mortgages work the same as traditional mortgages, HELOCs, or home equity loans

- Myth #10: Reverse mortgages are only for homeowners who plan to stay in their homes forever

- Myth #11: A reverse mortgage is a government benefit

- Myth #12: Reverse mortgages are too expensive to be worth it

- Myth #13: A reverse mortgage will affect my Social Security, Medicare, or taxes

- Myth #14: My spouse will lose the home if I pass away first

- What modern reverse mortgages actually look like today

- Frequently asked questions about reverse mortgage myths

Quick Answer: Many reverse mortgage myths are based on outdated information rather than how modern loans work today. Home Equity Conversion Mortgages (HECMs) include consumer safeguards designed to address many common concerns.

Key Points

HECMs include safeguards such as HUD-certified counseling, financial assessments, non-recourse protections, and protections for eligible non-borrowing spouses.1

Borrowers retain ownership of their homes and generally do not make required monthly mortgage payments, provided they continue paying property taxes, maintaining homeowners insurance, and keeping the home in good condition

Heirs generally have options when a reverse mortgage becomes due, including selling the home, refinancing the loan, or repaying the balance and keeping the property.

Are reverse mortgages a scam? Will the bank take your home? Can your children inherit debt? These are some of the most common reverse mortgage myths—and they often shape public perception long before homeowners ever consider one.

While reverse mortgages are not the right solution for every borrower, many common concerns are based on outdated information or misconceptions about how modern loans work. This guide separates fact from fiction and explains how today’s reverse mortgages work, including the consumer safeguards designed to protect borrowers and their families.

Myth #1: Reverse mortgages are risky or shady

Some consumers remain skeptical and may even wonder whether reverse mortgages are a scam. Many of these concerns are rooted in outdated information or experiences from earlier decades.

Like many financial products, reverse mortgage loans have evolved over time. In fact, the most common type of reverse mortgage, Home Equity Conversion Mortgage (HECM), includes a number of safeguards designed to help older homeowners make informed decisions and understand their responsibilities before moving forward with a loan.

One important safeguard is counseling. Before obtaining a HECM, borrowers are required to complete a session with an independent HUD-certified counselor. These counseling appointments are designed to explain how the loan works, discuss alternatives, review costs and obligations, and answer questions before a homeowner moves forward.

HECMs also include a financial assessment. Lenders evaluate factors such as income, assets, and credit history to help determine whether a borrower is likely to meet ongoing loan obligations, including paying property taxes, maintaining homeowners insurance, and keeping the home in good condition.

While no financial product is right for everyone, modern reverse mortgages are highly regulated and include safeguards that did not exist in many of the stories that continue to shape opinions today.

Myth #2: The bank takes your home

Perhaps the most persistent reverse mortgage myth is the lender takes ownership of the home. In reality, borrowers retain title to the property throughout the life of the loan.

Like a traditional mortgage, a reverse mortgage creates a lien against the home. This gives the lender a legal interest in the property as security, but it does not transfer ownership.

However, reverse mortgages do come with ongoing obligations. Borrowers are generally required to pay property taxes, maintain homeowners insurance, keep the home in good condition, and continue occupying the property as their principal residence. Failing to meet these obligations may cause the loan to become due and payable.

A reverse mortgage loan also becomes due and payable when the last borrower, or eligible non-borrowing surviving spouse, dies, sells the home, or permanently moves out of the property. At that point, the loan balance must be repaid, typically through the sale of the home or other available funds.

For federally insured HECMs, borrowers and their heirs are generally protected by the loan’s non-recourse feature. This means that if the loan balance exceeds the home’s value when the loan becomes due and the property is sold, neither the borrower nor the borrower’s estate will generally owe the difference, provided loan requirements have been met.1

Myth #3: You’ll still have monthly mortgage payments

One of the most well-known reverse mortgage advantages is that most borrowers are not required to make monthly mortgage payments on the loan balance. As long as the loan remains in good standing and the borrower continues meeting the loan’s requirements, interest and fees are generally added to the loan balance over time rather than paid each month.

However, eliminating monthly mortgage payments does not eliminate all homeowner responsibilities. Borrowers are required to pay property taxes, maintain homeowners insurance, keep the home in good condition, and continue occupying the property as their principal residence.

Some homeowners also choose to make voluntary payments on their reverse mortgage. While not required, these payments may reduce balance growth over time or help preserve more home equity for future needs or heirs.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

Myth #4: Most reverse mortgages end in foreclosure

While foreclosure may occur in some situations, it is not the typical outcome of a reverse mortgage loan.

Like any mortgage, a reverse mortgage comes with ongoing borrower obligations. Failing to meet these obligations may cause the loan to become due and payable and could ultimately result in foreclosure.

Many reverse mortgage misconceptions about foreclosure are based on stories from earlier decades, before a number of consumer safeguards were introduced. One example is the financial assessment requirement implemented in 2015, which helps evaluate a borrower’s ability to meet ongoing loan obligations. Around the same time, HUD expanded protections for eligible non-borrowing spouses, helping certain surviving spouses remain in their homes under specific circumstances.

Myth #5: My heirs will inherit debt, and I won’t leave anything to my children

Many reverse mortgage misconceptions involve inheritance. For federally insured HECMs, borrowers and heirs are protected by the loan’s non-recourse feature. This means one of the most common reverse mortgage myths—that children inherit reverse mortgage debt—is generally incorrect. Neither the borrower nor the borrower’s heirs are personally liable if the loan balance exceeds the value of the home when the loan becomes due and payable.1

When the last borrower or eligible non-borrowing surviving spouse dies, sells the home, or permanently moves out, the loan becomes due. At that point, heirs have several options. Depending on their circumstances, they may choose to:

- Sell the home and use the proceeds to repay the loan

- Refinance the loan into a traditional mortgage

- Repay the balance and keep the family home

- Walk away from the property

For HECMs, eligible heirs may also have the option to satisfy the loan by paying 95% of the home’s appraised value if the loan balance exceeds the home’s value.

Another common reverse mortgage myth is that a reverse mortgage automatically eliminates any inheritance. In reality, the amount of equity remaining depends on several factors, including home appreciation, loan balance growth, and how long the loan remains outstanding.

For example, if the home is worth more than the reverse mortgage loan balance when it is sold, any remaining proceeds may go to the borrower’s heirs.

Myth #6: You can’t move or sell your home

Some homeowners worry that obtaining a reverse mortgage means giving up the ability to move or sell their home. In reality, borrowers generally remain free to do both if their circumstances change.

Like a traditional mortgage, a reverse mortgage is secured by the property. If the home is sold, the loan balance is typically repaid from the sale proceeds, and any remaining equity belongs to the homeowner or the homeowner’s estate.

In most cases, reverse mortgages also do not include prepayment penalties, meaning borrowers may repay the loan at any time without incurring an additional fee.

Myth #7: You need perfect finances to be eligible for a reverse mortgage

Many homeowners assume they need excellent credit and perfect finances to be eligible for a reverse mortgage. In reality, HECM eligibility requirements differ from those used for many traditional forward mortgages.

Borrowers may still be eligible if they have an existing mortgage, provided they have sufficient home equity. In many cases, reverse mortgage proceeds are first used to pay off the existing mortgage or other eligible liens secured by the property.

Rather than focusing primarily on income and debt ratios, reverse mortgage lenders generally place greater emphasis on factors such as age, available home equity, and a borrower’s ability to meet ongoing loan obligations.

→ Learn more: What are reverse mortgage eligibility requirements?

Myth #8: Reverse mortgages are only for people in financial distress or as a last resort

While some borrowers use reverse mortgages to address immediate financial needs, others incorporate them into broader retirement planning strategies.

Depending on their circumstances, many retirees use reverse mortgage proceeds for a variety of purposes, including:

- Supplementing retirement cash flow

- Funding home modifications that support aging in place

- Paying for caregiving or in-home care services

- Establishing an emergency reserve for unexpected expenses

→ Read more about planning for aging in place in our guide: How to age in place.

The right to remain in the home is contingent on paying property taxes and homeowners insurance, maintaining the home, and complying with the loan terms.

Myth #9: Reverse mortgages work the same as traditional mortgages, HELOCs, or home equity loans

Because reverse mortgages, HELOCs, and home equity loans all allow homeowners to access home equity, many people assume they work the same way. In reality, they operate differently and are designed for different purposes.2

One of the biggest differences involves how repayment works and when the loan becomes due. With a traditional mortgage, home equity loan, or HELOC, borrowers are generally required to make monthly payments. Most reverse mortgage borrowers, by contrast, are not required to make monthly mortgage payments as long as they continue meeting the loan’s obligations. Interest and fees generally accrue over time and are added to the loan balance.

A reverse mortgage loan also becomes due and payable under different circumstances. Repayment is generally triggered when the borrower sells the home, permanently moves out of the property, dies, or otherwise fails to meet the loan’s requirements.

Another key difference is how funds may be received. Depending on the product and borrower preferences, reverse mortgages may offer several payout options, including:

- A lump-sum payment

- A line of credit

- Monthly payments or advances

- A combination of payment options

Some reverse mortgage lines of credit also include a growth feature that may increase available borrowing capacity over time, provided loan requirements are met. This feature differs from many traditional borrowing products and may provide additional flexibility for some homeowners.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

→ Explore further: Reverse mortgage vs HELOC vs home equity loan.

Myth #10: Reverse mortgages are only for homeowners who plan to stay in their homes forever

Many reverse mortgage myths assume these loans are only appropriate for homeowners who intend to remain in the same property for the rest of their lives. While reverse mortgages are often associated with aging in place, some homeowners use them as part of broader housing and retirement plans.

Homeowners who decide to move are generally not trapped by the loan. If the home is sold, the reverse mortgage loan is typically repaid from the sale proceeds, and any remaining equity belongs to the homeowner or the homeowner’s estate.

The right to remain in the home is contingent on paying property taxes and homeowners insurance, maintaining the home, and complying with the loan terms.

Myth #11: A reverse mortgage is a government benefit

The connection to FHA and HUD often leads homeowners to believe a reverse mortgage is a government benefit rather than a loan.

While FHA insurance and HUD oversight help establish product requirements and consumer protections, they do not mean a reverse mortgage is a government grant, entitlement, or public assistance benefit. Instead, the borrower is accessing a portion of the equity that already exists in their home through a loan.

FHA insurance also supports important consumer protections, including the non-recourse protections available through federally insured HECMs.1

Myth #12: Reverse mortgages are too expensive to be worth it

Cost is one of the biggest concerns homeowners raise when evaluating a reverse mortgage. Like many mortgage products, reverse mortgages may include origination fees, FHA mortgage insurance premiums (for HECMs), and third-party closing costs such as appraisal, title, and recording fees.

In many cases, some or all of these costs may be financed into the loan rather than paid out of pocket at closing. Whether a reverse mortgage is worth the cost depends on a homeowner’s goals, circumstances, and how the loan is used.

→ Dive deeper: Reverse mortgage fees and costs explained.

Another reverse mortgage misconception is that there is a single answer to whether the loan is cost-effective. In reality, the value calculation may depend on several factors, including:

- How long the homeowner expects to remain in the property

- How the proceeds are used

- Whether the borrower chooses a lump sum, line of credit, or another payment option

- Changes in home value and available equity over time

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

Myth #13: A reverse mortgage will affect my Social Security, Medicare, or taxes

In most cases, reverse mortgage proceeds are considered loan proceeds rather than income. As a result, they generally do not affect Social Security or Medicare eligibility.

However, some needs-based government programs, like Medicaid and Supplemental Security Income (SSI), may consider assets and available resources when determining eligibility. In certain situations, reverse mortgage proceeds that are retained in a bank account beyond the month they are received could affect eligibility.

Reverse mortgage proceeds are generally not considered taxable income. At the same time, reverse mortgage interest is generally not deductible until the loan is partially or fully repaid.

Because tax situations and government benefit rules vary, homeowners should consider consulting qualified financial, tax, or benefits professionals when evaluating how a reverse mortgage may affect their individual circumstances.

Myth #14: My spouse will lose the home if I pass away first

Many homeowners worry that a surviving spouse will automatically be forced to leave the home if the borrowing spouse dies first. Modern HECMs include protections for certain eligible non-borrowing spouses that may allow them to remain in the home after the death of the borrowing spouse, provided program requirements are met.

However, these protections do not apply to everyone, and eligibility depends on factors such as marital status, loan terms, and other program requirements.

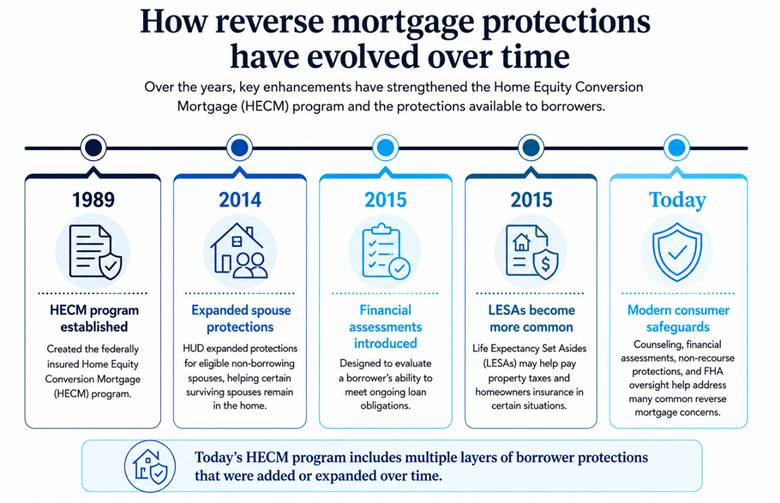

What modern reverse mortgages actually look like today

Many common reverse mortgage myths are rooted in outdated information. Today’s HECMs generally include multiple consumer safeguards designed to help borrowers make informed decisions and understand their responsibilities.

Today’s HECMs generally include:

- Independent counseling

- Financial assessments

- Non-recourse protections

- Protections for eligible non-borrowing spouses

- Multiple payout options

The graphic below highlights several key milestones that helped shape the modern HECM program and the consumer safeguards available today.

To learn more, please visit the CFPB’s “Reverse Mortgage: A Discussion Guide.”

While reverse mortgages are not the right solution for every homeowner, understanding the facts may help you evaluate whether they fit your financial goals, housing plans, and retirement strategy.

If you’re considering a reverse mortgage, a calculator may help you estimate available proceeds and explore different borrowing scenarios based on your age, home value, and location.

→ Try Finance of America’s reverse mortgage calculator

Frequently asked questions about reverse mortgage myths

Are reverse mortgages a scam?

No. Reverse mortgages are legitimate loan products regulated by federal and state regulations. While reverse mortgages are not the right solution for every homeowner, modern HECMs include safeguards such as counseling requirements, financial assessments, non-recourse protections, and FHA oversight.1

What happens if I outlive the reverse mortgage?

Reverse mortgages do not have a fixed repayment term. As long as you continue meeting the loan’s requirements, you may remain in the home.

What happens if I fall behind on property taxes or homeowners insurance?

Failing to meet required loan obligations may cause the loan to become due and payable. If the issue is not resolved, foreclosure may occur. This is one reason modern HECMs include financial assessments and, in some cases, LESAs.

Can heirs keep a home with a reverse mortgage?

Yes. In many cases, heirs may choose to repay the loan balance and keep the home, refinance the loan, or sell the property and keep any remaining equity after the loan is repaid.

Can a reverse mortgage affect inheritance for my children?

Yes. Because loan balances generally increase over time, a reverse mortgage may reduce the amount of home equity available to heirs. However, it does not automatically eliminate an inheritance, and any remaining equity belongs to the homeowner or the homeowner’s estate.

What happens if home values decline?

For federally insured HECMs, borrowers and heirs are generally protected by the loan’s non-recourse feature. This means they cannot owe more than the home’s value when the loan becomes due and the property is sold, provided loan requirements are met.1

Do reverse mortgages require monthly mortgage payments?

Most reverse mortgage borrowers are not required to make monthly mortgage payments on the loan balance. However, they must continue meeting the loan’s ongoing obligations.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

1Non-recourse means that you, or your estate, can’t owe more than the value of your home when the loan becomes due and the home is sold.

Non-recourse means that if you default on the loan, or if the loan cannot otherwise be repaid, the lender cannot look to your other assets (or your estate’s assets) to meet the outstanding balance on your loan.

2Finance of America does not currently offer home equity loans.

About the author

is a Senior Web Content Writer at Finance of America and a journalist with more than 20 years of experience specializing in business, and technology. Her work has been published in The Wall Street Journal, The Financial Times, and numerous other leading outlets.

Disclaimer

This article is intended for general informational and educational purposes only and should not be construed as financial or tax advice. For tax advice, please consult a tax professional. For more information about whether a reverse mortgage fits into your retirement strategy, you should consult your financial advisor.