Explore by category

Reverse mortgage pros and cons: What to consider before deciding

In this article:

Quick Answer: A reverse mortgage provides access to home equity with no required monthly mortgage payments, provided loan requirements are met. Potential drawbacks include costs, interest that increases the balance over time, and reduced equity for heirs.

Key Points

A reverse mortgage may help eligible homeowners turn a portion of their home equity into cash—but interest, fees, and loan terms affect how much remains over time.

FHA-insured HECMs follow federal guidelines and include consumer safeguards. However borrowers must meet eligibility requirements and continue paying property taxes, maintaining homeowners insurance, and keeping the home in good condition.

The right choice depends on your financial goals, how long you plan to stay in your home, and your overall retirement strategy.

Even if you don’t know much about reverse mortgages, you’ve probably heard a few warnings about them—perhaps that the bank takes your home, that your children inherit debt, or that reverse mortgages are a scam.

The reality is more nuanced. Like any financial product, reverse mortgages have both advantages and tradeoffs. For some homeowners, reverse mortgages may provide greater financial flexibility during retirement. For others, the costs, obligations, or long-term impact on home equity may outweigh any potential advantages.

Understanding the reverse mortgage pros and cons may help homeowners separate common misconceptions from reality and make a more informed decision about whether a reverse mortgage fits into their retirement plans.

What is a reverse mortgage?

A reverse mortgage is a loan that may allow eligible homeowners to turn a portion of their home equity into funds while continuing to live in the home. Unlike a traditional mortgage, most reverse mortgage borrowers are not required to make monthly mortgage payments on the loan balance, provided they continue to meet the loan’s requirements.

Borrowers are generally required to continue paying property taxes, maintaining homeowners insurance, keeping the home in good condition, and occupying the home as their principal residence.

Reverse mortgage proceeds may be received as a lump sum, monthly payments, a line of credit, or a combination of payment options. Interest and fees accrue over time and are added to the loan balance, which grows throughout the life of the loan. The loan typically becomes due and payable when the borrower sells the home, permanently moves out, dies, or otherwise fails to meet the loan’s requirements.

The most common type of reverse mortgage is the Home Equity Conversion Mortgage (HECM), which the FHA insures. Proprietary reverse mortgages offered by private lenders may provide additional borrowing options for some homeowners. In contrast, single-purpose reverse mortgages are typically offered by certain government agencies or nonprofit organizations for specific uses.

To learn more, please visit the CFPB’s “Reverse Mortgage: A Discussion Guide”

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

Reverse mortgage pros

Like any financial product, reverse mortgages offer both advantages and tradeoffs. The right solution depends on your goals, financial situation, and long-term plans. Here are some of the most commonly cited pros of getting a reverse mortgage.

→ Learn more: 15 reverse mortgage facts

No required monthly mortgage payments

One core advantage of a reverse mortgage is that borrowers are not required to make monthly mortgage payments on the loan balance. For retirees on fixed incomes, eliminating a required mortgage payment may help improve cash flow and free up room in the monthly budget for other expenses.

However, borrowers may choose to make voluntary payments. While not required, voluntary payments may reduce loan balance growth over time or preserve more home equity for future needs or heirs.

This differs from many home equity loans and home equity lines of credit (HELOCs), which generally require monthly payments. With a reverse mortgage, interest and fees accrue over time and are added to the loan balance rather than being paid each month.1

However, borrowers must continue meeting the loan’s ongoing obligations, including paying property taxes, maintaining homeowners insurance, keeping the home in good condition, and occupying the home as their principal residence.

→ Take a closer look: Reverse mortgage vs HELOC vs home equity loan: Comparing your home equity options

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

Access home equity while staying in your home

Another reverse mortgage advantage is the ability to access home equity without selling your home. For homeowners who want to remain in their current residence, a reverse mortgage may provide funds to support aging in place.

Unlike selling the property or downsizing, a reverse mortgage allows borrowers to retain ownership of the home. Homeowners remain responsible for paying property taxes, maintaining homeowners insurance, keeping the home in good condition, and occupying the property as their principal residence.

This flexibility may be appealing to homeowners who want access to additional funds while continuing to live in a familiar home and community. Depending on individual goals and circumstances, reverse mortgage proceeds may be used for a variety of purposes, including home modifications, healthcare expenses, or other retirement needs.

→ Read more: How to age in place: A planning guide for homeowners

The right to remain in the home is contingent on paying property taxes and homeowners insurance, maintaining the home, and complying with the loan terms.

Flexible payout options

Reverse mortgage funds may be received as a lump sum, monthly payments, a line of credit, or a combination of payment options.

This flexibility allows homeowners to select a payout structure that aligns with their financial goals and anticipated expenses. For example, some borrowers prefer monthly payments to supplement retirement income, while others might choose a line of credit that may be accessed as needed.

One of the more unique features of a HECM line of credit is that any unused portion of the available credit line may grow over time, provided loan requirements continue to be met. The growth rate is tied to the same rate used to calculate growth on the loan balance, including the applicable annual mortgage insurance premium. Importantly, this growth feature is not dependent on future home appreciation.

In addition, HECM lines of credit generally cannot be frozen, reduced, or canceled solely because home values decline, provided the borrower continues meeting the loan’s obligations.

Reverse mortgages may support retirement flexibility

One reason some homeowners consider a reverse mortgage is the flexibility to use proceeds for a variety of retirement needs:

- Supplement retirement income

- Pay off an existing mortgage

- Cover healthcare or long-term care expenses

- Fund home remodeling projects, repairs, or accessibility updates

- Help family members financially

- Preserve other retirement savings and liquid assets

- Support lifestyle goals that may improve retirement quality of life

For some homeowners, accessing a portion of their home equity may provide additional financial flexibility during retirement. Rather than relying exclusively on investment accounts, savings, or other assets, they choose a reverse mortgage as part of their broader retirement strategy.

Non-recourse protections (HECMs only)

Because HECMs are insured by the FHA, borrowers and their heirs are generally protected from owing more than the home’s value when the loan becomes due and payable and the property is sold, provided loan requirements have been met.2

For example, if the loan balance exceeds the home’s value when the reverse mortgage is due, neither the borrower nor the borrower’s estate will be responsible for paying the difference.

However, it is important to understand that non-recourse protections apply to federally insured HECMs and may not apply to other reverse mortgage products. Homeowners considering a proprietary reverse mortgage should carefully review the loan terms and any applicable borrower protections.

Heirs may still inherit the home

One common misconception about reverse mortgages is that heirs automatically lose the home. In reality, when a reverse mortgage becomes due and payable, heirs have several options:

- Sell the home and use the proceeds to repay the loan

- Refinance the reverse mortgage into a traditional mortgage and keep the home

- Repay the loan balance and retain ownership of the property

For federally insured HECMs, eligible heirs may also have the option to satisfy the loan by paying 95% of the home’s appraised value if the loan balance exceeds the home’s value when the loan becomes due. This protection works alongside the loan’s non-recourse feature and may provide additional flexibility for families who wish to keep the home.2

While a reverse mortgage may reduce the amount of home equity available over time, it does not automatically prevent heirs from inheriting the home or retaining ownership of the property.

Built-in consumer safeguards

Many of the reverse mortgage pros available through federally insured HECMs stem from the program’s additional consumer safeguards.

Before obtaining a HECM, borrowers are generally required to complete an independent session with a counselor certified by the U.S. Department of Housing and Urban Development (HUD). Counseling sessions are intended to help prospective borrowers better understand the loan’s costs, obligations, and alternatives.

HECMs are also subject to rules established by the FHA, which help standardize the program and provide important borrower protections. In addition, current HECM rules include protections for eligible non-borrowing spouses, which may allow certain surviving spouses to remain in the home after the death of the borrowing spouse if product requirements are met.

In most cases, reverse mortgages do not include prepayment penalties, meaning borrowers may repay the loan early without incurring an additional fee.

Reverse mortgage proceeds are usually tax-free

Reverse mortgage proceeds are a loan, not income. As a result, reverse mortgage proceeds are generally not subject to federal income tax. This may provide additional flexibility for homeowners who want to supplement retirement cash flow without generating taxable income by selling assets.

However, tax situations vary from person to person. Homeowners should consult with a qualified tax professional to discuss the tax implications of a reverse mortgage.

Reverse mortgage cons

While reverse mortgages offer multiple potential advantages, they also involve costs, obligations, and tradeoffs that may make them less suitable for some homeowners. Understanding the most common reverse mortgage cons may help you evaluate whether a reverse mortgage aligns with your financial goals, housing plans, and long-term retirement strategy.

Reverse mortgages may reduce available home equity over time

One of the most important reverse mortgage cons to understand is that the loan balance generally grows over time as interest and applicable fees are added.

As the loan balance grows, available home equity generally decreases. The longer a reverse mortgage remains outstanding, the greater the potential impact on remaining equity.

For homeowners who plan to leave their home to their heirs, this reduction in equity may be an important consideration. While heirs may still have options when the loan becomes due, less equity may remain in the home over time.

The extent of the impact depends on several factors, including how much is borrowed, interest rates, changes in the home value, and the length of the loan.

There are upfront and ongoing costs

Another potential reverse mortgage drawback is cost. Like many mortgage products, reverse mortgages may include upfront expenses and ongoing charges, which you should consider when evaluating whether the loan aligns with your financial goals.

Depending on the loan product and property, costs may include:

- Origination fees

- Closing costs

- Upfront and ongoing mortgage insurance premiums (for HECMs)

- Counseling fees, where applicable

- Ongoing servicing fees, where applicable

Some of these costs may be financed into the loan rather than paid out of pocket at closing. However, financed costs are added to the loan balance, which may reduce available home equity and the proceeds available to the borrower from the outset.

Because costs vary based on the loan, property, and borrower circumstances, homeowners should carefully review all fees before moving forward with a reverse mortgage.

→ Learn more: Reverse mortgage fees and costs explained

You’ll still have ongoing property obligations

A common misconception is that obtaining a reverse mortgage eliminates the responsibilities associated with homeownership. In reality, borrowers must continue meeting several ongoing obligations throughout the life of the loan, including:

- Paying property taxes

- Maintaining homeowners insurance

- Paying applicable homeowners association (HOA) dues

- Keeping the home in good condition

While most reverse mortgage borrowers are not required to make monthly mortgage payments on the loan balance, failing to meet these obligations may cause the loan to become due and payable. In some situations, foreclosure may occur if the borrower does not meet the loan requirements.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

Needs-based benefits may be affected

While reverse mortgage proceeds are generally treated as loan proceeds rather than income, they may affect eligibility for certain needs-based government programs.

Programs such as Medicaid, Supplemental Security Income (SSI), and the Supplemental Nutrition Assistance Program (SNAP) may consider your assets and available resources when determining eligibility. If reverse mortgage proceeds remain in a bank account, they may be counted as an asset when determining eligibility.

As a result, homeowners who currently receive needs-based benefits, or who expect to apply for them in the future, should carefully consider how reverse mortgage proceeds may affect their eligibility.

Reverse mortgages are more complex than traditional loans

Reverse mortgages involve unique rules, repayment triggers, and long-term considerations that may make them more complex than many traditional borrowing products. As a result, homeowners should take time to understand how the loan works and how it may fit into their broader financial plans.

For federally insured HECMs, borrowers are generally required to complete counseling with a counselor certified by the U.S. Department of Housing and Urban Development (HUD). These sessions are designed to explain how the loan works, review alternatives, discuss borrower obligations, and answer questions before a homeowner moves forward.

Many homeowners also consult with financial advisors, tax professionals, or other trusted professionals when evaluating their reverse mortgage options. Family conversations may be helpful as well, particularly when inheritance goals, caregiving needs, or long-term housing plans are important considerations.

In addition, homeowners should compare reverse mortgages with other available options, including home equity lines of credit (HELOCs), home equity loans, cash-out refinances, downsizing, and other borrowing strategies. Understanding the advantages, tradeoffs, costs, and eligibility requirements of each option may help homeowners determine which approach best aligns with their needs.1

→ Learn more: What is a reverse mortgage and how does it work?

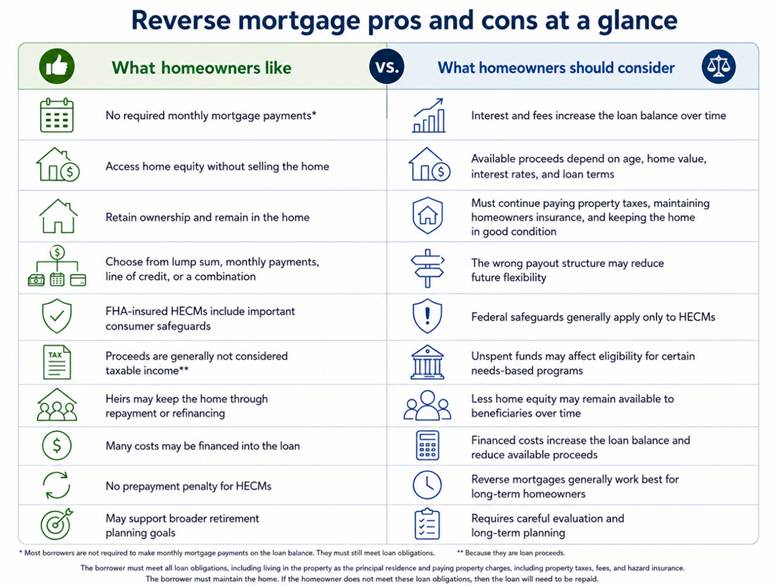

For a quick side-by-side summary, see the infographic below.

How to decide if a reverse mortgage is right for you

These reverse mortgage pros and cons illustrate why the loan is not a one-size-fits-all solution. Whether a reverse mortgage makes sense depends on your financial goals, housing plans, available resources, and long-term needs.

Homeowners evaluating a reverse mortgage should also understand the reverse mortgage process, including counseling requirements, financial assessment, property valuation, loan closing, and ongoing borrower obligations.

Situations where a reverse mortgage may make sense

A reverse mortgage may be worth exploring for homeowners who plan to remain in their homes long term, which is typically five years or more. Because of upfront costs and a loan balance that grows over time, these loans are generally better suited for homeowners with longer time horizons.

Reverse mortgages are frequently considered by retirees living on fixed incomes or those seeking greater cash-flow flexibility during retirement. They may also appeal to homeowners who want to pay off an existing mortgage and reduce monthly expenses, age in place, or preserve other retirement savings and investment assets.

Depending on individual circumstances, reverse mortgage proceeds may help fund healthcare expenses, long-term care needs, home repairs, accessibility updates, or other major expenses.

The right to remain in the home is contingent on paying property taxes and homeowners insurance, maintaining the home, and complying with the loan terms.

Situations where a reverse mortgage may be less suitable

Conversely, homeowners who plan to move in the near future may find that other options are more appropriate, since reverse mortgages are generally designed for longer-term homeowners.

These loans may also be less appealing to homeowners who want to leave their homes debt-free to heirs or who are uncomfortable with a loan balance that generally grows over time. In addition, homeowners who may have difficulty paying property taxes, maintaining homeowners insurance, paying HOA dues, or keeping the home in good condition should carefully evaluate their ability to meet the loan’s ongoing obligations.

Finally, homeowners with limited home equity or access to other funding sources may find that a reverse mortgage isn’t the best fit.

The graphic below offers a side-by-side summary of these considerations.

→ Dive deeper: Is a reverse mortgage a good idea?

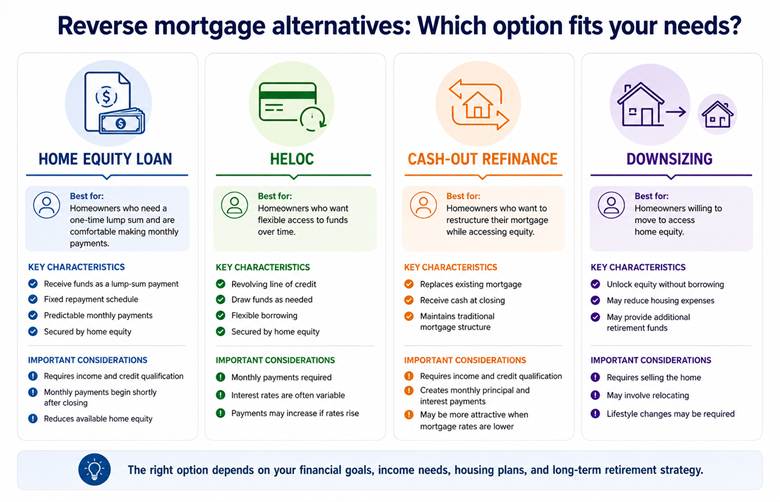

Reverse mortgage alternatives

A reverse mortgage is only one way to access home equity or to create additional financial flexibility during retirement. Depending on your goals, financial situation, and long-term plans, other borrowing, housing, or retirement funding strategies may be worth considering as well.

Understanding how reverse mortgages compare with other options may help you evaluate the advantages, tradeoffs, costs, and eligibility requirements of each approach.

Home equity loan

A home equity loan allows homeowners to borrow against their available home equity and receive the funds as a lump-sum payment. Unlike a reverse mortgage, home equity loans generally require regular monthly payments that begin shortly after the loan closes.1

Because home equity loans are repaid over a fixed term, borrowers typically have predictable monthly payments and a defined repayment schedule. However, lenders generally evaluate factors such as income, credit history, and debt obligations when determining borrower eligibility.

For homeowners who need a one-time lump sum and are comfortable making monthly payments, a home equity loan may be an alternative worth considering.

HELOC

A home equity line of credit (HELOC) is a revolving line of credit secured by the equity you have in your home. Unlike a home equity loan, which provides a lump sum upfront, a HELOC allows borrowers to draw funds as needed up to an approved credit limit.

HELOCs typically require monthly payments, and the amount due may vary depending on the outstanding balance and applicable interest rate. Many HELOCs also have variable interest rates, which means borrowing costs and monthly payments may increase or decrease over time as market rates change.

For homeowners who need flexible access to funds and are comfortable making monthly payments, a HELOC may be an alternative to consider when comparing home equity borrowing options.

→ Dive deeper: Is a HELOC a good idea? Here’s how to decide

Cash-out refinance

A cash-out refinance replaces an existing mortgage with a new mortgage for a larger amount, allowing the homeowner to receive the difference in cash. Because the transaction restructures the mortgage, the borrower begins making monthly principal and interest payments under the terms of the new loan.

Unlike a reverse mortgage, a cash-out refinance typically requires income and credit qualification and creates an immediate monthly payment obligation. However, it may be an attractive option for homeowners who qualify and want to access home equity while maintaining a traditional mortgage structure.

In some situations, a cash-out refinance may be particularly appealing when current mortgage rates are lower than the homeowner’s existing rate. Conversely, refinancing into a higher rate could increase borrowing costs and monthly payments.

Downsizing

For some homeowners, downsizing may be an alternative to a reverse mortgage. By selling a larger home and purchasing a smaller or less expensive property, homeowners may be able to unlock home equity without borrowing against the property.

Depending on housing costs and market conditions, downsizing may reduce ongoing expenses such as mortgage payments, property taxes, insurance costs, maintenance, and utility bills. It may also provide additional cash to support retirement goals or other financial needs.

However, downsizing may require homeowners to leave a long-time residence, relocate to a new community, or adjust to a smaller living space. As a result, the decision often involves both financial and lifestyle considerations.

The graphic below summarizes these considerations side by side:

How to compare reverse mortgage pros and cons

The right way to evaluate a reverse mortgage is to consider how it fits into your broader retirement and housing plans. While the advantages and drawbacks may provide a useful starting point, every homeowner’s situation is different.

When comparing reverse mortgage pros and cons, consider the following questions:

- What are your long-term retirement goals and priorities?

- How long do you expect to remain in your home?

- How does a reverse mortgage fit into your retirement income strategy and cash-flow needs?

- What are your inheritance goals, and how important is preserving home equity for heirs?

- Have you discussed the decision with family members, financial advisors, counselors, or other trusted professionals?

- How does a reverse mortgage compare with other options, such as a home equity loan, HELOC, cash-out refinance, downsizing, or other retirement funding strategies?1

For homeowners still exploring their options, Finance of America’s reverse mortgage calculator may provide a helpful starting point. Ultimately, the best choice depends on your goals, financial circumstances, and long-term plans. Taking time to compare options and evaluate tradeoffs may help you determine whether a reverse mortgage aligns with your needs.

FAQs

What are the biggest pros and cons of a reverse mortgage?

Common reverse mortgage pros include no required monthly mortgage payments, access to home equity while remaining in the home, and flexible payout options. Common cons include loan balance growth over time, upfront costs, ongoing property obligations, and potential reduction in available home equity for heirs.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

Will I still own my home with a reverse mortgage?

Yes. Borrowers retain ownership of the home and continue holding title to the property. However, they must continue paying property taxes, maintaining homeowners insurance, keeping the home in good condition, and occupying the home as their principal residence.

Do reverse mortgages require monthly mortgage payments?

Most reverse mortgage borrowers are not required to make monthly mortgage payments on the loan balance. However, they remain responsible for paying property taxes, maintaining homeowners insurance, and keeping the home in good condition.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

How much can you borrow with a reverse mortgage?

How much equity you have in your home is one of the primary factors used to determine available proceeds. The available loan amount also depends on factors such as age, home value, interest rates, and loan type. Because every homeowner’s situation is different, borrowing amounts vary.

Who is eligible for a reverse mortgage?

For HECMs, borrowers generally must be at least 62 years old, occupy the home as their principal residence, have sufficient home equity, and meet applicable program requirements. Borrowers must also continue paying property taxes, maintaining homeowners insurance, and keeping the home in good condition throughout the life of the loan.

What costs and fees come with a reverse mortgage?

Depending on the loan, costs may include origination fees, closing costs, mortgage insurance premiums, counseling fees where applicable, and servicing fees where applicable. Some or all of these costs may be financed into the loan.

Can you lose your home with a reverse mortgage?

Borrowers generally retain ownership of the home throughout the life of the loan. However, failing to meet loan obligations may cause the loan to become due and payable and could ultimately result in foreclosure.

What happens if home values decline after getting a reverse mortgage?

For federally insured HECMs, borrowers and heirs are generally protected by the loan’s non-recourse feature. This means they are not personally liable for any difference between the loan balance and the home’s value when the loan becomes due, provided loan requirements are met.2

What happens to a reverse mortgage when the homeowner dies?

When the last borrower or eligible non-borrowing surviving spouse dies, the loan generally becomes due and payable. The loan balance is then typically repaid through the sale of the home or other available funds.

What happens to a spouse who is not a borrower?

For federally insured HECMs, certain eligible non-borrowing spouses may be able to remain in the home after the borrowing spouse dies, provided product requirements are met. These protections do not automatically apply to every household member, so homeowners should carefully review spouse and survivor considerations before obtaining a reverse mortgage.

Can heirs keep a home with a reverse mortgage?

Yes. Heirs may choose to repay the loan balance, refinance the loan, or sell the property. For federally insured HECMs, eligible heirs may also have the option to satisfy the loan by paying 95% of the home’s appraised value if the loan balance exceeds the home’s value.

How long do you have to repay a reverse mortgage?

A reverse mortgage does not have a fixed repayment term. Repayment generally occurs when the borrower sells the home, permanently moves out, dies, or otherwise fails to meet the loan’s requirements.

How does a reverse mortgage compare with a HELOC or home equity loan?

All three options allow homeowners to access home equity, but they work differently. Home equity loans and HELOCs generally require monthly payments and income qualification, while most reverse mortgage borrowers are not required to make monthly mortgage payments on the loan balance.1

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

Does a reverse mortgage affect Social Security or Medicare?

In most cases, reverse mortgage proceeds are considered loan proceeds rather than income and generally do not affect Social Security or Medicare eligibility. However, certain needs-based programs such as Medicaid, SSI, or SNAP may be affected if proceeds remain unspent and are treated as assets.

Are reverse mortgages a good idea for retirees on fixed incomes?

They may be for some retirees. One reason homeowners consider reverse mortgages is the ability to access home equity without required monthly mortgage payments on the loan balance.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

When does a reverse mortgage make sense?

A reverse mortgage may make sense for homeowners who plan to remain in their homes long term, have substantial home equity, want greater retirement cash-flow flexibility, or wish to age in place. The right solution depends on a homeowner’s goals, financial circumstances, and long-term plans.

The right to remain in the home is contingent on paying property taxes and homeowners insurance, maintaining the home, and complying with the loan terms.

1Finance of America does not currently offer home equity loans.

2Non-recourse means that you, or your estate, can’t owe more than the value of your home when the loan becomes due and the home is sold. Non-recourse means that if you default on the loan, or if the loan cannot otherwise be repaid, the lender cannot look to your other assets (or your estate’s assets) to meet the outstanding balance on your loan.

About the author

is a Senior Web Content Writer at Finance of America and a journalist with more than 20 years of experience specializing in business, and technology. Her work has been published in The Wall Street Journal, The Financial Times, and numerous other leading outlets.

Disclaimer

This article is intended for general informational and educational purposes only and should not be construed as financial or tax advice. For tax advice, please consult a tax professional. For more information about whether a reverse mortgage fits into your retirement strategy, you should consult your financial advisor.