Explore by category

HELOC vs. HECM–Which is right for you?

In this article:

- How does a home equity conversion mortgage (HECM) work?

- How does a home equity line of credit (HELOC) work?

- What are the differences between a HECM reverse mortgage and a HELOC?

- HECM vs. HELOC: A practical example

- When might a HECM be the better choice?

- When might a HELOC be the better choice?

- Are there other home equity loan options?

- Final thoughts: Which home equity option is right for you?

- Frequently Asked Questions: HELOC vs. HECM

Key points

A HECM is an FHA-insured reverse mortgage that eliminates monthly mortgage payments and is available only to homeowners age 62 and older. *

A HELOC requires ongoing monthly payments and is available to homeowners of any age if they meet the lender’s financial requirements.

Both loans may be right for you depending on your financial situation, needs, and whether you meet the specific qualifications.

American households held $34.5 trillion in home equity in the first quarter of 2025, according to LendingTree. That’s a $600 billion jump from just a year earlier.

For many homeowners, especially those nearing or in retirement, that equity may serve as a financial safety net. But deciding between a home equity line of credit (HELOC) and a home equity conversion mortgage (HECM) to access your equity can be challenging.

Both options unlock cash from your home’s equity—but they also come with trade-offs that could strain cash flow and create stress.

If you’re weighing a HELOC vs. HECM reverse mortgage and feeling stuck, you’re in the right place. Let’s look at how each option works, where they differ, and when one might be a better fit.

*The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

How does a home equity conversion mortgage (HECM) work?

A HECM is an Federal Housing Administration (FHA)-insured reverse mortgage for homeowners age 62 and older. It may allow you to convert a portion of your home equity into cash without taking on an additional monthly mortgage payment.

Instead of making payments to a lender, as you would in a traditional mortgage, the reverse mortgage loan balance is disbursed to you. This balance increases over time and must be repaid when you die, move out of the home, or otherwise fail to meet the loan terms. Often, the loan is repaid by selling the home. Still, borrowers and their heirs also have other options, like refinancing or paying off the loan to keep the home.

Here are the key things to know about HECMs:

- No required monthly mortgage payments: The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

- Multiple ways to receive funds: Borrowers have flexible options for how to receive proceeds—as a lump sum, in monthly payments, as a line of credit, or a combination of these methods. (Depending on your loan structure, you may or may not be able to choose your payout method. For example, fixed-rate HECMs must be taken as a lump sum.)

- Required counseling: Before you can apply for a HECM, you must attend a counseling session with a HUD-approved counselor to ensure you understand the terms and conditions of the loan. You will pay for the session out of pocket.

- Growing line of credit: If you choose the HECM line of credit, the unused portion grows over time, giving you access to greater borrowing capacity in the future—even if your home value stays the same or declines.

- Non-recourse protection: A HECM is a non-recourse loan, meaning neither you nor your heirs will ever owe more than the home’s value at the time the loan becomes due, even if the loan balance exceeds it.

- Ongoing homeowner responsibilities: While there are no required monthly mortgage payments, borrowers must continue to pay property taxes and homeowners insurance and maintain the home to keep the loan in good standing.

It’s worth noting that HECMs are not the only type of reverse mortgage, but they are strictly regulated and require mandatory counseling, have capped costs, and include federal insurance providing added borrower protections but with greater restrictions. To learn more, visit the CFPB’s Reverse Mortgage: A Discussion Guide.

A non-recourse reverse mortgage transaction limits the homeowner’s liability to the proceeds of the sale of the home (or any lesser amount specified in the credit obligation). Non-recourse means that you, or your estate, can’t owe more than the value of your home when the loan becomes due and the home is sold. Non-recourse means that if you default on the loan, or if the loan cannot otherwise be repaid, the lender cannot look to your other assets (or your estate’s assets) to meet the outstanding balance on your loan.

→To learn more about home equity conversion mortgage, read our in-depth guide What is a HECM?.

How does a home equity line of credit (HELOC) work?

A home equity line of credit (HELOC) lets you borrow against your home’s equity on an as-needed basis, similar to a credit card, but with your home as collateral. Unlike a lump-sum loan, a HELOC gives you a revolving credit line you can draw from, repay, and draw from again during the draw period—typically 5 to 10 years. It’s available to homeowners of any age who meet credit and income requirements, and monthly payments are required from the start. Because your home secures the loan, failure to repay could put it at risk.

A HELOC has two main phases. The first is the draw period, which typically lasts 5 to 10 years. During this time, you may access funds up to your approved credit limit, repay what you borrow, and continue drawing again as needed. Most HELOCs require monthly interest-only payments on the amount borrowed in this window.

After the draw period ends, the HELOC enters the repayment phase. At this point, you must begin repaying both principal and interest over a set term. Because you’re now paying down both principal and interest, monthly payments are typically higher—which can catch borrowers off guard if they haven’t planned ahead.

Here are a few other things to understand about HELOCs:

- Payments are required: Unlike a HECM, a HELOC requires ongoing monthly payments. Even during the draw period, you’ll typically make interest payments, which may impact cash flow, especially for retirees on fixed incomes.

- Rates are usually variable: HELOC interest rates are commonly tied to a benchmark like the prime rate. As a result, your payments may increase over time if interest rates go up.

- Access to funds may change: Lenders may freeze or reduce a HELOC if your financial situation changes, your credit profile declines, or broader housing market conditions worsen, so access to funds isn’t always guaranteed.

- Credit and income matter: Approval and terms are heavily influenced by credit score, income, and debt-to-income ratio. Strong ongoing income is generally required to qualify and maintain the credit line.

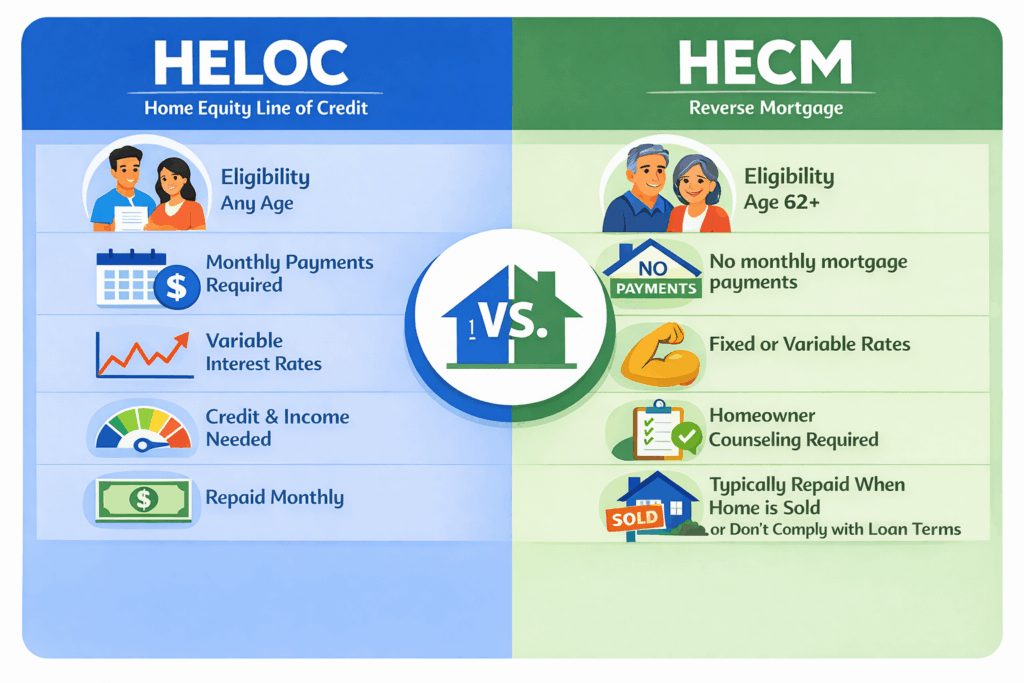

What are the differences between a HECM reverse mortgage and a HELOC?

While both a HECM and HELOC allow borrowers to access home equity, they work very differently. This table covers the core differences between the two loan options, and we’ll explore them in more detail below.

| Category | HECM (Reverse Mortgage) | HELOC |

| Eligibility | Age 62+, primary residence, meets FHA home standards, HUD-approved counseling required. Credit and income assessment required. | Any age. Strong credit, steady income, and manageable debt-to-income ratio required. |

| Monthly payments | No required monthly mortgage payments.* | Monthly payments required on borrowed amount. |

| Financial obligations | Interest and mortgage insurance accrue monthly and are added to the loan balance. Borrowers must pay property taxes and insurance and maintain the home. | Interest (and sometimes principal) must be paid monthly, reducing cash flow. |

| How funds are received | Lump sum (fixed-rate), monthly payments, line of credit, or a combination. | Revolving credit line during draw period. |

| Interest rates | Fixed or variable. Fixed rate requires a lump sum; variable rate offers more flexibility. | Typically variable and tied to a market index. |

| Repayment timing | Due when the home is sold, the borrower permanently moves, passes away, or fails to meet loan terms. | Ongoing repayment during draw period; full repayment or refinance after draw period ends. |

*The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

What are the eligibility requirements for a HECM vs. HELOC?

To be eligible for a HECM, at a minimum, borrowers must be at least 62 years old and live in the home as their primary residence. The home must meet FHA property standards, and borrowers must complete HUD-approved counseling before closing.

Credit and income are reviewed as part of a financial assessment to ensure you can meet ongoing property obligations like paying insurance and property taxes. You’ll also need sufficient equity in your home—typically at least 50%. However, the exact amount depends on your age, current interest rates, and any existing mortgage balance.

HELOC eligibility is generally less age-restrictive but requires stronger financial qualifications. Borrowers typically need strong credit, sufficient income, and a manageable debt-to-income ratio. Lenders also look closely at employment and cash flow, since monthly payments are required. HELOCs are generally available to homeowners of any age who meet these financial criteria.

→ Learn more in our guide How much equity do you need for a reverse mortgage?

How do the financial obligations differ between a HECM vs. HELOC?

This is one of the biggest differences between a HECM and a HELOC.

With a HECM, borrowers are not required to make monthly mortgage payments. Instead, interest and mortgage insurance costs accrue over time and are added to the loan balance. Borrowers continue to pay property taxes and homeowners insurance and maintain the home. As long as those obligations are met and the home remains the primary residence, no monthly loan payments are due.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

With a HELOC, borrowers are required to make monthly payments throughout the life of the loan. During the draw period, those payments typically cover interest and may include some principal.

During the repayment period, borrowers make interest and principal payments, which are often much higher than during the draw period. These required payments reduce monthly cash flow, which is an important consideration for retirees or anyone on a fixed income.

How do you receive funds from a HELOC vs. HECM?

With a HELOC, borrowers access funds through a revolving credit line. You may draw money as needed during the draw period, up to the approved limit. As you repay what you borrow, those funds become available again. Once the draw period ends, no new funds may be accessed, and repayment terms change.

With a HECM, borrowers may have several options for loan disbursement. Funds can generally be taken as a lump sum, fixed monthly payments, a line of credit with increasing borrowing capacity, or a combination of these options. Many borrowers like the HECM line of credit because it remains available as long as loan obligations are met and unused funds may grow, increasing borrowing capacity over time.

How do HECM and HELOC interest rates compare?

HECMs and HELOCs approach interest very differently, and the structure matters just as much as the rate itself. With a HECM, borrowers may choose either a fixed or variable (adjustable) interest rate.

- Fixed-rate HECMs require a one-time, lump-sum disbursement and offer a stable interest rate, which works well for a single, immediate need for cash.

- Variable-rate HECMs allow more flexibility, including lines of credit and monthly payments, and often come with lower initial rates and higher available borrowing amounts.

As of early 2026, fixed HECM rates generally range from 7.6% to 7.9%, though they can vary by lender and location. Variable-rate HECMs typically start with lower initial margins.

With a HELOC, interest rates are usually variable and tied to a market index. Borrowers pay interest only on the amount they draw, and payments are required monthly. As of January 2026, HELOC rates are approximately 6.2% to 8%, but may also vary by credit score, location, and lender.

Rates are subject to change and vary based on borrower profile, market conditions, and loan structure.

When does a HECM or HELOC need to be repaid?

With a HECM, the loan does not come due as long as the borrower lives in the home as a primary residence and continues to meet loan obligations, such as paying property taxes, fees, homeowners insurance, and maintaining the home.

HECM loans become due when triggering events occur, such as the borrower permanently moving out, passing away, or otherwise failing to meet loan requirements. At that point, typically the home is sold to repay the loan, though heirs may choose other options.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

With a HELOC, repayment is ongoing and required. During the draw period, borrowers must make monthly payments, usually covering interest and sometimes principal. After the draw period ends—usually 5 to 10 years—the loan enters a repayment phase that can result in higher monthly payments. These required payments may strain cash flow, especially for borrowers on a fixed income.

HECM vs. HELOC: A practical example

There are quite a few differences between the two loan types, as you can see. Let’s look at a practical example to compare how the two loans work. (Note: These figures are illustrative and assume steady home appreciation and repayment on the HELOC over several years.)

Imagine Susan, a 67-year-old retiree who wants to access her home equity. She owns her home, which is currently valued at $400,000.

If Susan chooses a HECM:

Susan applies for and is approved for a HECM. She receives $100,000 in loan proceeds in a lump sum, which she uses to make repairs to her home and take several trips with her friends. Over time, interest and mortgage insurance accrue, increasing the loan balance.

Susan remains responsible for property taxes, homeowners insurance, and home maintenance. Ten years later, Susan decides to relocate closer to her adult children and she sells the home, repays the HECM, and keeps $250,000 in remaining equity, which she uses for a down payment on a smaller home.

This loan scenario has been prepared for illustrative purposes only and is based on the hypothetical borrower and loan assumptions noted below. Loan terms potentially available to a borrower are based upon factors such as home value, mortgage payoffs, location, age, interest rates and payment plan chosen, and credit profile.

If Susan chooses a HELOC:

Susan applies for and is approved for a HELOC of $100,000. She draws $40,000 from the line of credit to make repairs to her home and later withdraws another $5,000 to take an Alaskan cruise. Because a HELOC requires ongoing repayment, Susan makes monthly interest payments for 7 years, then starts making larger principal and interest payments once it enters the repayment period.

Over time, Susan’s loan balance decreases as she makes payments. She remains responsible for property taxes, homeowners insurance, and maintenance. Ten years later, Susan decides to relocate closer to her adult children and sells the home. She uses the sale proceeds to pay off the HELOC balance of $20,000 and keeps the remaining $380,000 in equity, which she uses as a down payment on a smaller property.

When might a HECM be the better choice?

A HECM may be a better fit for older homeowners who want to access home equity without taking on new monthly mortgage payments. It often works well for retirees on a fixed income who want to supplement cash flow or establish a flexible line of credit as a financial safety net.

A HECM may also make sense if flexibility matters more than a set repayment schedule. For example, the HECM line of credit allows you to borrow and repay, then borrow again. If you choose monthly payout options, you’ll receive predictable loan disbursements every month.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

When might a HELOC be the better choice?

A HELOC may be a better fit for homeowners with steady income who are comfortable making required monthly payments. It often works well for those who are still working and have a clear plan to repay what they borrow over time.

A HELOC may also make sense when funds are needed for a specific purpose, such as home renovations or other planned expenses. The line of credit allows you to borrow, repay, and borrow again during the draw period. Still, monthly payments are required, and interest rates are typically variable.

Are there other home equity loan options?

Yes. Depending on your age, income, goals, and how you plan to use the funds, one of these alternatives may be a better fit.

- Proprietary reverse mortgages: These are non-government-insured reverse mortgages offered by private lenders. They’re typically designed for homeowners with higher-value homes and may allow access to more equity than a HECM, but they don’t include FHA insurance protections. Jumbo reverse mortgages are a common type of proprietary reverse mortgage.

- Home equity loans: Often called a “second mortgage,” a home equity loan provides a one-time lump sum with fixed monthly payments over a set term. This option works best for borrowers with strong income and credit who want predictable payments.

- Cash-out refinance: This replaces your existing mortgage with a new, larger loan and gives you the difference in cash. While it may offer lower interest rates than some equity products, it requires monthly payments on the full loan amount and extends the term of your loan.

- Personal loans or other financing options: For smaller or short-term needs, unsecured loans may be an option, though they often come with higher interest rates and shorter repayment terms.

Final thoughts: Which home equity option is right for you?

Both HECMs and HELOCs offer ways to access home equity, but they’re built for very different financial situations.

A HELOC may be a better fit if you:

- Have steady income and are comfortable making monthly payments

- Need funds for a short-term or specific expense

- Plan to repay the balance over time

- Expect to sell or refinance within a defined timeframe

A HECM reverse mortgage may be a better fit if you:

- Are age 62 or older

- Want to access home equity without adding a monthly mortgage payment

- Are retired or focused on preserving cash flow

- Plan to stay in your home long term

- Value flexible options like a line of credit or monthly payments

Curious about how much you might be eligible for with a reverse mortgage? Use our reverse mortgage calculator.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

Frequently Asked Questions: HELOC vs. HECM

Is a reverse mortgage or a HELOC cheaper?

A HELOC often has lower upfront costs but requires monthly payments that add up over time. A reverse mortgage has higher upfront costs, including mortgage insurance, but no required monthly mortgage payments, which may reduce long-term cash-flow strain for retirees. Whether one is cheaper depends entirely on your specific circumstances.

Is a HELOC considered a reverse mortgage?

No. A HELOC is a traditional loan that requires monthly repayment. A reverse mortgage, including a HECM, does not require monthly mortgage payments and is designed specifically for older homeowners.

Can I get a HECM with bad credit?

Yes, in most cases. A HECM does not require a minimum credit score. Credit and income are reviewed to determine whether you may meet ongoing obligations like property taxes, homeowners insurance, and maintenance, not to qualify you for monthly payments.

Is a HELOC better than a reverse mortgage for seniors?

It depends on your income and cash flow. A HELOC may be a better option if you have steady income and are comfortable making monthly payments. A reverse mortgage may be a better fit if you want to access home equity without adding a monthly mortgage payment.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

Is a HELOC cheaper than a HECM?

A HECM includes higher initial expenses, such as an upfront mortgage insurance premium equal to 2% of the home’s value, plus ongoing mortgage insurance. However, a HELOC requires monthly payments, which may cost more over time depending on how long you carry the balance and interest rates. One is not inherently cheaper than the other.

About the author

Danielle Antosz

Danielle Antosz is the Web Content Manager at Finance of America and a journalist with more than 10 years of experience whose work has appeared in MoneyWise, MSN, Yahoo! Finance, and The Motley Fool. She specializes in making complex financial topics accessible and is passionate about advancing financial literacy.

Disclaimer

This article is intended for general informational and educational purposes only and should not be construed as financial or tax advice. For tax advice, please consult a tax professional. For more information about whether a reverse mortgage fits into your retirement strategy, you should consult your financial advisor.