Explore by category

How long does it take to get a reverse mortgage?

Quick Answer: It generally takes 30 to 60 days to apply and receive loan proceeds from a reverse mortgage. However, it may take longer depending on your circumstances.

Key Points

The reverse mortgage timeline typically takes 30 to 60 days and involves 5 steps including counseling, filling out the loan application, home appraisal and inspection, underwriting, and closing.

Several things can delay the process, including delays in scheduling counseling or appraisal, if repairs are required, and complex situations that require more documentation.

To limit delays, make sure to have documentation organized, address repairs quickly, and stay in contact with your lender.

If you’re considering a reverse mortgage, one of the first questions you likely have is: How long will it take to get my money? The answer might be shorter than you expect.

The reverse mortgage process typically takes one to two months from application to funding—though timing may vary based on your situation and how quickly each step moves. Before we dive into the timeline, let’s first cover the basics about a reverse mortgage so you understand how it may impact your long-term goals.

Understanding reverse mortgages

A reverse mortgage is a loan that may allow older homeowners to convert a portion of their home equity into cash without requiring them to move out or sell their home. Instead, loan disbursements are sent to the borrower as a lump sum, a line of credit, or monthly installments.

As long as the borrower lives in the home for more than half of the year, maintains the home, and pays property taxes, insurance, and other fees, no monthly mortgage payment is required. When the last surviving borrower (or eligible non-borrowing spouse) dies, moves out of the home, or can no longer meet loan terms, it becomes due.

The most popular type of reverse mortgage loan is the Home Equity Conversion Mortgage (HECM), which is federally insured by the Federal Housing Administration (FHA). To be eligible, you must at minimum:

- Be 62+ years old

- Live in the home as your primary residence

- Have substantial home equity

- Meet financial assessment requirements

Proprietary reverse mortgages, like jumbo reverse mortgages, are not backed by federal regulations, but do follow a similar timeline. They may have different eligibility requirements, which can vary by lender.

→See how Linda used the proceeds of the reverse mortgage on her historic San Francisco home to reduce financial stress.

The reverse mortgage process timeline

In most cases, a reverse mortgage takes 30 to 60 days from application to funding. During that time, the process moves through five main steps: HUD-approved counseling (required for HECMs), application and document submission, home appraisal, underwriting and financial assessment, and closing with funding.

Counseling and appraisal scheduling tend to drive the early pace, while underwriting complexity and title clearance shape the back half. Staying in close contact with your lender and scheduling counseling early are the two most effective ways to keep your loan on track.

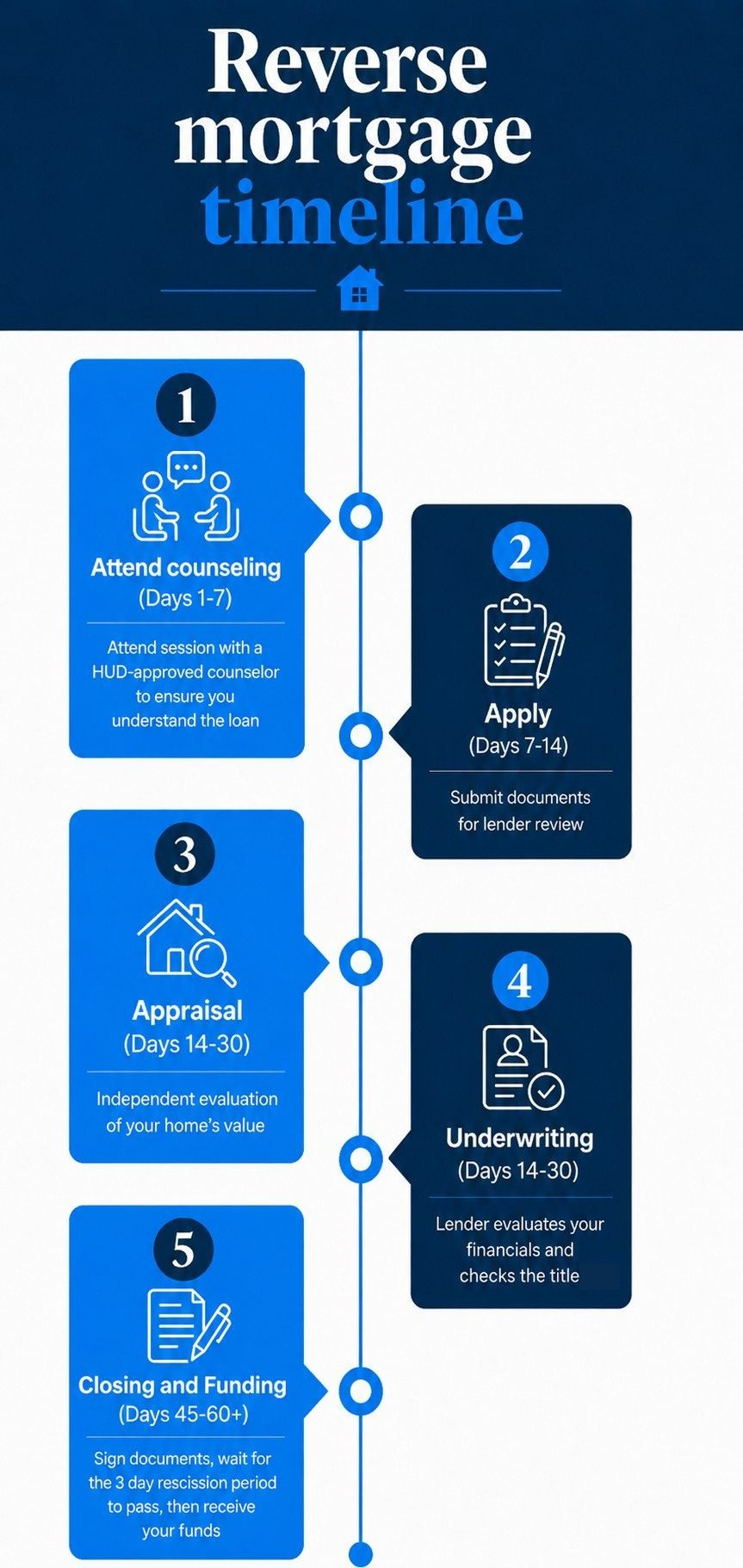

The image below outlines what to expect at each stage and about how long it typically takes:

Counseling is required for HECM loans.

Step 1: Mandatory counseling (Days 1-7)

Anyone who applies for a HECM reverse mortgage loan must complete a counseling session with a HUD-approved third-party counselor. This ensures you understand the reverse mortgage requirements and have a chance to ask questions and explore other options so you can make an informed financial decision. Most proprietary reverse mortgages also require this counseling during the decision-making process, but it varies by lender.

You can find a list of HUD-approved counselors in your area on the HUD website or through the Consumer Financial Protection Bureau (CFPB). Because scheduling can take time, scheduling your session early can help avoid delays.

Step 2: Select a lender and fill out the loan application (Days 7-14)

In this stage, you submit a formal application to the lender of your choice. You’ll need to provide documents that verify your date of birth, proof of income, Social Security number, homeowner’s insurance, and a mortgage statement.

The lender may ask for additional information to ensure you meet the loan’s eligibility requirements. They will also run a title search on the home to ensure there are no federal liens present.

This is also when you’ll learn how much you might be eligible to borrow based on your home’s value, the age of the youngest borrower, and current interest rates. Additional eligibility factors may also apply.

→ Learn more about the application process in our guide, How to apply for a reverse mortgage in 5 steps

Step 3: Home appraisal and inspection (Days 14-30)

The appraisal determines your home’s value and may impact how much you’re able to borrow. An independent, third-party appraiser will do a walkthrough to determine your home’s value and ensure it meets the minimum property standards for a reverse mortgage.

In some cases, the appraisal may take only a couple of days, but it could take up to two weeks or longer, depending on local appointment availability.

Step 4: Underwriting and financial assessment (Days 30-45)

Before the loan moves forward, your reverse mortgage lender will perform a financial assessment that looks at your income, credit history, and property charges. The goal of this assessment is to ensure you can continue to pay for insurance, taxes, and maintenance. It may impact the terms of your reverse mortgage loan.

Then, the loan moves into underwriting. The reverse mortgage underwriting process usually takes about 10 to 15 days, but it may take longer if the underwriter requires additional documentation.

Step 5: Closing and reverse mortgage funding (Days 45-60)

If you are approved, the loan closing process is similar to a traditional mortgage. You’ll meet with a notary to sign the reverse mortgage documents and confirm the paperwork matches the terms you discussed with your loan officer, including the loan amount, fees, interest rate, and the disbursement of loan proceeds.

Once you receive your signed closing documents and meet any final conditions, there is a waiting period before any funds may be disbursed called the three-day right of rescission. This gives you an opportunity to cancel the loan if you change your mind.

On the fourth business day, any current mortgages or property liens are paid off. A percentage of the remaining funds may be disbursed to you at that time.

To learn more, please visit the Consumer Financial Protection Bureau’s (CFPB’s Reverse Mortgage: A Discussion Guide.

What can delay a reverse mortgage application?

While the reverse mortgage process is designed to be straightforward, several factors can cause delays:

- If your required counseling session is delayed due to scheduling issues.

- If local appraisers are in high demand.

- If your property requires repairs to meet FHA minimum property standards.

- If the lender needs additional documentation during underwriting, or if your financial situation is complex.

- If the home has existing liens or unresolved title issues.

Being proactive can help you get a reverse mortgage with fewer delays and access your loan proceeds sooner.

How can you speed up the reverse mortgage process?

You may be able to shorten your reverse mortgage timeline by being prepared and responsive to your lender. Here are a few other ways to speed up the process:

- Schedule counseling immediately: Book your HUD-approved session as soon as you decide to apply.

- Gather documents up front: Have your ID, income records, insurance, and mortgage statements ready before applying. Make sure to have the most recent versions of each type of paperwork.

- Address property issues early: Resolve any obvious repair needs before the appraisal. For example, patching the roof or replacing missing deck boards.

- Stay responsive: Reply to lender requests within 24-48 hours whenever possible. This ensures they are able to keep the process moving.

- Choose an experienced lender: Working with a lender who specializes in reverse mortgages may speed up the process because specialized teams have experience that may help them process applications more efficiently.

Why choose Finance of America?

With decades of experience in home equity solutions for older homeowners, Finance of America works to streamline the process and reduce unnecessary delays. Our dedicated reverse mortgage professionals understand the nuances of these loans and work closely with you to help ensure everything moves forward as efficiently as possible.

From your first conversation through closing, our team prioritizes clear communication so you always understand what’s happening and what to expect next. If you’re exploring whether a reverse mortgage fits your needs, an experienced, supportive lender may make all the difference.

To get a personalized estimate of what you might be eligible for, try our reverse mortgage calculator.

Frequently asked questions about reverse mortgage loans

Why are there required counseling sessions for reverse mortgage loans?

Counseling sessions for a reverse mortgage are required to help you evaluate whether a reverse mortgage is the right loan for you. Your counselor will explain how reverse mortgages work, including payment options, pros and cons, and tax implications.

What is the longest a reverse mortgage can take?

The reverse mortgage process can extend to 90 days or more due to complex situations involving title issues, property repairs, or extensive documentation.

How is a HECM reverse mortgage different from other reverse mortgage loans?

A HECM is federally regulated and offers borrower safeguards like required counseling with a HUD-approved counselor, a maximum borrower amount, and non-recourse protection, which means you or your heirs will never owe more than the house is worth.1

What are the different ways to receive reverse mortgage funds?

The disbursement options vary depending on the type of reverse mortgage you choose, but generally include a lump sum, line of credit, monthly disbursements, or a combination of those options. Not all options are available in all states.

Does the type of reverse mortgage affect the timeline?

Yes. HECMs follow the standard FHA timeline, while proprietary reverse mortgages like HomeSafe may have slightly different timing depending on the lender.

What happens after I sign the closing documents?

You have a three-business-day right of rescission. On the fourth business day, existing mortgages are paid off and any remaining proceeds are disbursed.

Can I withdraw from a reverse mortgage after closing?

Yes. Federal law gives you three business days after closing to cancel without penalty. This period is called the right of rescission.

1 Non-recourse means that if you default on the loan, or if the loan cannot otherwise be repaid, the lender cannot look to your other assets (or your estate’s assets) to meet the outstanding balance on your loan.

About the author

is the Web Content Manager at Finance of America and a journalist with more than 10 years of experience whose work has appeared in MoneyWise, MSN, Yahoo! Finance, and The Motley Fool. She specializes in making complex financial topics accessible and is passionate about advancing financial literacy.

Disclaimer

This article is intended for general informational and educational purposes only and should not be construed as financial or tax advice. For tax advice, please consult a tax professional. For more information about whether a reverse mortgage fits into your retirement strategy, you should consult your financial advisor.