Explore by category

What are the three types of reverse mortgage loans?

In this article:

Quick Answer: The three types of reverse mortgage include Home Equity Conversions mortgages (HECM), proprietary reverse mortgages, and single-purpose reverse mortgages. The different types may have different eligibility requirements, loan terms, and borrower safeguards.

Key points

There are three main types of reverse mortgages: HECM, proprietary, and single-purpose reverse mortgages. Each type of reverse mortgage may have different requirements and loan terms, so understanding the differences is important to making an informed decision.

The most common type of reverse mortgage, the HECM, is insured by the FHA and has specific rules and borrower safeguards set by federal agencies.

Proprietary reverse mortgages allow lenders to offer more flexible terms, while single-purpose reverse mortgages are offered by local agencies and non-profits for one defined purpose.

The reverse mortgage industry is growing rapidly. According to Grand View Research, the global reverse mortgage market was valued at $1.83 billion in 2023 and is projected to reach $2.71 billion by 2030. As interest in these loans grows, it’s more important than ever to understand how reverse mortgages work.

A reverse mortgage may allow older homeowners to convert part of their home equity into cash without requiring monthly mortgage payments. Instead, repayment is typically deferred until the borrower sells the home, moves out permanently, or passes away. To keep the loan in good standing, borrowers must also meet the loan terms, which include living in the home as their primary residence, maintaining the home, and paying property taxes and homeowners insurance.

Many people assume all reverse mortgages are the same, but there are actually several types with different eligibility requirements, payout options, and borrowing limits. Whether you’re considering a reverse mortgage for yourself or helping a loved one evaluate their options, this guide explains the different types of reverse mortgages and how they work.

What are the 3 reverse mortgage loan options?

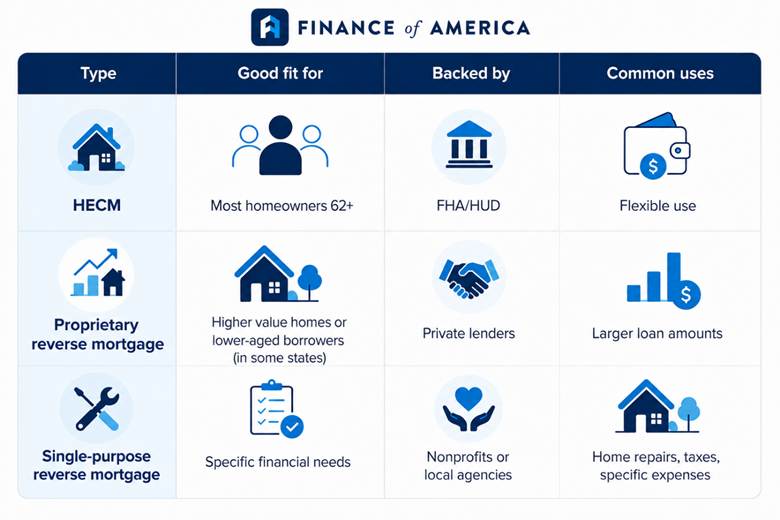

There are three main types of reverse mortgages: Home Equity Conversion Mortgages (HECMs), proprietary reverse mortgages, and single-purpose reverse mortgages. Each option is designed for different financial needs, home values, and goals.

The most common option is the HECM, which is insured by the Federal Housing Administration (FHA). Proprietary reverse mortgages are private loans often used for higher-value homes. Single-purpose reverse mortgages are less common and are typically offered by local governments or nonprofits for approved expenses like home repairs or property taxes.

Here’s a quick comparison of the three reverse mortgage types:

Note: The age requirement for all HECMs is 62+. Some proprietary reverse mortgages may have lower age requirements in some states. Qualification varies by state and lender.

To learn more, please visit the Consumer Financial Protection Bureau’s (CFPB) Reverse Mortgage: A Discussion Guide.

HECM: The most common type

HECMs are the most widely used type of reverse mortgage. They are insured by the FHA and regulated by the U.S. Department of Housing and Urban Development (HUD), which provides borrower safeguards and standardizes lending rules.

To be eligible, borrowers must meet several guidelines, including:

- At least one borrower must be 62 years old or older.

- The home must serve as the borrower’s primary residence.

- The borrower must have significant equity, often at least 50%.

- The borrower must be able to continue paying property taxes, homeowners insurance, and home maintenance costs.

- Complete a counseling session with a HUD-approved housing counselor to ensure you understand the costs, responsibilities, repayment rules, and alternatives.

Like other reverse mortgages, HECMs allow homeowners to convert a portion of their home equity into cash without required monthly mortgage payments. Repayment is generally deferred until the borrower sells the home, permanently moves out, or passes away.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

HECM loans are also subject to a federal lending limit, known as the maximum claim amount. For 2026, the national HECM lending limit is $1,249,125, meaning homeowners cannot borrow more than that amount, no matter how much home equity they have.

One of the key protections offered through HECM loans is the non-recourse feature. This means neither the borrower nor their heirs will owe more than the home’s value when the loan becomes due, even if the loan balance eventually exceeds the property value.

Non-recourse means that you, or your estate, can’t owe more than the value of your home when the loan becomes due, and the home is sold. Non-recourse means that if you default on the loan, or if the loan cannot otherwise be repaid, the lender cannot look to your other assets (or your estate’s assets) to meet the outstanding balance on your loan.

→ Learn more about reverse mortgage requirements: What are reverse mortgage eligibility requirements?

Proprietary reverse mortgages (jumbo): For higher-value homes

Proprietary reverse mortgages are private loans offered by individual lenders rather than government-backed programs. Because they are not insured by the FHA or regulated under HECM rules, lenders have more flexibility.

Common features of proprietary reverse mortgages vary by product, but may include:

- Higher borrowing limits than federally insured HECM loans (jumbo reverse mortgages)

- Eligibility for some borrowers as young as 55 in some states

- No upfront or monthly mortgage insurance premiums (MIPs)

- Greater flexibility in loan structures and payout options

Jumbo reverse mortgages, a common type of proprietary reverse mortgage, are designed for homeowners with higher-value properties that exceed the FHA lending limits for HECM loans. However, jumbo loans are not the only type of proprietary reverse mortgage. Some lenders also offer specialized products with different qualification standards, age requirements, or property guidelines depending on the borrower’s financial situation and home value.

Unlike HECMs, proprietary reverse mortgages do not generally require upfront or ongoing mortgage insurance premiums, which may reduce some loan costs. However, interest rates and fees may be higher, depending on the lender and loan structure.

Another major difference is eligibility age. While HECMs require at least one borrower to be age 62 or older, some proprietary reverse mortgage products extend eligibility to borrowers as young as 55 in some states.

Because these loans are privately structured, borrower protections, fees, and repayment terms may vary, so make sure you fully understand the loan if you choose a proprietary reverse mortgage.

Learn more about HomeSafe, a suite of jumbo reverse mortgage options from Finance of America.

The HomeSafe reverse mortgage is a proprietary product of Finance of America and is not related to the Home Equity Conversion Mortgage (HECM) program. HomeSafe products are only available in certain states. Please contact us for a complete list of availability.

Single-purpose reverse mortgage: Designed for specific expenses

Single-purpose reverse mortgages are the least common type. These are typically offered by local governments, nonprofit organizations, or community programs and have limited availability. Unlike HECMs and proprietary reverse mortgages, where borrowers have flexible use of their funds, they are intended for a specific use.

Single-purpose reverse mortgages often have lower costs and may have less strict financial requirements than other reverse mortgage options. However, they are not available in all areas. These loans are commonly offered to older, lower-income homeowners for things like:

- Home repairs or accessibility upgrades

- Property taxes

- Homeowners insurance

- Deferred home maintenance

- Energy efficiency improvements

Eligibility requirements vary by product, and borrowers typically cannot use the money for general living expenses, travel, or to get a handle on debt, like they could with other reverse mortgages.

→ Is a reverse mortgage a good idea? Learn more in our guide: Are reverse mortgages good or bad?

HECM vs jumbo reverse mortgage

For most homeowners comparing reverse mortgage options, the decision typically comes down to a federally insured HECM loan or a proprietary jumbo reverse mortgage. While both allow homeowners to convert home equity into cash without required monthly mortgage payments, they differ in borrowing limits, eligibility requirements, costs, and borrower protections.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

We didn’t include single-purpose reverse mortgages in this comparison because they are much less common and their requirements, loan limits, and approved uses can vary significantly from location to location.

Let’s break down the main differences:

| Feature | HECM reverse mortgage | Proprietary/jumbo reverse mortgage |

| Backing | Federally insured by FHA/HUD | Private lender product |

| Age requirement | Homeowners age 62+ | Varies; may be available to homeowners age 55+ in some states |

| Maximum loan amount | Subject to FHA lending limits | Higher borrowing limits for high-value homes |

| Mortgage insurance premiums (MIP) | Required upfront and annually | Not required |

| HUD counseling requirement | Required with HUD-approved counselor | Often not required by lender, but not mandatory by law |

| Government safeguards | Includes FHA borrower protections and standardized rules | None; Protections vary by lender |

| Non-recourse protection | Included | Often included, but terms vary by lender |

| Interest rates | Often competitive and standardized | May be higher depending on lender and loan type |

| Property types allowed | Must meet FHA property requirements | May offer more flexibility |

| Suited for | Most eligible homeowners 62+ | Higher-value homes that exceed FHA lending limits, or younger borrowers in some states |

Understanding fees and closing costs

The cost of a reverse mortgage can vary significantly based on the type of loan you choose. One of the biggest differences between HECM and proprietary reverse mortgages is mortgage insurance.

Because HECM loans are federally insured by the FHA, borrowers are required to pay mortgage insurance premiums. These costs typically include both an upfront payment at closing and an ongoing annual premium that accrues over time. In exchange, borrowers receive federal safeguards, including non-recourse protection and guaranteed access to loan funds.

Proprietary reverse mortgages, including many jumbo reverse mortgage products, are not regulated by the federal government and do not require FHA mortgage insurance premiums. This may reduce upfront costs for some borrowers, particularly homeowners with higher-value properties. However, proprietary loans may carry higher interest rates and may not offer the same borrower safeguards.

Other reverse mortgage costs may include:

- Origination fees

- Appraisal and closing costs

- Title insurance

- Interest charges

- Servicing fees, if applicable

Another important factor to understand is negative amortization. Since reverse mortgage borrowers are not required to make monthly mortgage payments, interest and fees are added to the loan balance over time. As the balance grows, the homeowner’s remaining equity gradually decreases. This applies to all types of reverse mortgages.

→ Learn more about reverse mortgage costs and fees.

The borrower must meet all loan obligations, including living in the property as the principal residence and paying property charges, including property taxes, fees, and hazard insurance. The borrower must maintain the home. If the homeowner does not meet these loan obligations, then the loan will need to be repaid.

How reverse mortgages are repaid

With a reverse mortgage, loan repayment is typically deferred until specific events occur. The loan becomes due when the borrower:

- Sells the home

- Permanently moves out of the home

- Passes away

- Fails to meet loan obligations, such as paying property taxes, homeowners insurance, or maintaining the property

When the loan becomes due, heirs typically have several options. They may repay the loan balance and keep the home, sell the home and use the proceeds to pay off the reverse mortgage, or walk away and allow the lender to sell the property.

For federally insured HECM loans, non-recourse protections ensure that neither the borrower nor their heirs will owe more than the home’s value at the time the loan is repaid.

→ Wondering what a reverse mortgage means for your heirs? Learn more: Are heirs responsible for reverse mortgage debt?

Choosing the right reverse mortgage type for you

The right reverse mortgage option depends on your age, home value, financial goals, and how you plan to use the funds. Before choosing a loan, it helps to ask a few key questions:

- How much home equity do I have?

- Is my home value above the FHA HECM lending limit?

- Do I want the protections of a federally insured loan?

- How much cash do I need to access?

- Am I comfortable paying mortgage insurance premiums?

- Do I want flexible access to funds or money for a specific purpose?

- Am I borrowing for myself, or helping a parent evaluate options?

- How long do I plan to remain in the home?

In general, a HECM reverse mortgage is often the best fit for homeowners who want federally backed protections, standardized loan rules, and flexible payout options.

A proprietary or jumbo reverse mortgage may make more sense for homeowners with higher-value properties who want to access more equity than FHA lending limits allow.

A single-purpose reverse mortgage may be worth considering for homeowners who only need help covering a specific expense, such as home repairs or property taxes, and who are eligible for a local nonprofit or government program.

Next steps

Reverse mortgages are not one-size-fits-all loans. From federally insured HECMs to jumbo proprietary products and single-purpose loans, each option is designed for different financial situations and goals. Understanding how these loans work and how they differ may help homeowners and their families make more informed decisions about using home equity in retirement.

For many borrowers, the next step is determining how much cash they might be able to access. Use our reverse mortgage calculator to estimate borrowing power, explore payout options, and see which type of reverse mortgage may fit your needs.

→ Use our reverse mortgage calculator to see how much you may be eligible for.

FAQ section

What is the most popular reverse mortgage option?

The most common reverse mortgage is the HECM. HECM loans are federally insured by the FHA and regulated by HUD, which gives borrowers standardized protections, counseling requirements, and flexible payout options.

How much equity is required for a reverse mortgage?

Most reverse mortgage borrowers need significant home equity, typically at least 50%. The exact amount depends on factors like the borrower’s age, home value, current mortgage balance, and the type of reverse mortgage.

What is the difference between fixed-rate and adjustable-rate reverse mortgages?

A fixed-rate reverse mortgage has an interest rate that stays the same for the life of the loan. These loans often require borrowers to take funds as a lump sum. An adjustable-rate reverse mortgage has an interest rate that may change over time based on market conditions. Adjustable-rate loans typically offer more flexible payout options, such as monthly payments or a line of credit.

Who owns the house with a reverse mortgage?

The homeowner still owns the home with a reverse mortgage. The lender does not take ownership as long as the borrower continues meeting loan requirements, including living in the home as a primary residence and staying current on property taxes, homeowners insurance, and maintenance.

Can I cancel a reverse mortgage after closing?

Yes. HECM borrowers have a three-business-day right of rescission after closing. This means borrowers may cancel the reverse mortgage for any reason within three business days of signing the final loan documents without penalty.

What happens to my spouse if they aren’t on the reverse mortgage?

HUD provides protections for eligible non-borrowing spouses on HECM loans. If the borrowing spouse passes away, an eligible non-borrowing spouse may be allowed to remain in the home without immediately repaying the loan, provided they continue meeting the loan requirements and the home remains their primary residence.

About the author

is the Web Content Manager at Finance of America and a journalist with more than 10 years of experience whose work has appeared in MoneyWise, MSN, Yahoo! Finance, and The Motley Fool. She specializes in making complex financial topics accessible and is passionate about advancing financial literacy.

Disclaimer

This article is intended for general informational and educational purposes only and should not be construed as financial or tax advice. For tax advice, please consult a tax professional. For more information about whether a reverse mortgage fits into your retirement strategy, you should consult your financial advisor.