Explore by category

Reverse mortgage loan-to-value ratios explained

In this article:

Quick answer: A loan-to-value (LTV) ratio compares a mortgage balance to a home’s value. A higher LTV means a larger loan relative to the property’s value, while a lower LTV means the borrower has more home equity.

Key points

A lower LTV generally means more home equity, while a higher LTV means a larger portion of the home’s value is tied to debt.

Home Equity Conversion Mortgages (HECMs) use principal limit factors (PLFs) and Federal Housing Administration (FHA) lending limits to determine how much may be available through the loan.

Understanding principal limits and home equity may help homeowners estimate potential reverse mortgage proceeds.

When you’re researching a reverse mortgage, you’re likely to encounter a lot of unfamiliar acronyms: Home Equity Conversion Mortgage (HECM), Life Expectancy Set Aside (LESA), Total Annual Loan Cost (TALC), and loan-to-value (LTV), just to name a few.

Some of these terms describe loan features or product requirements. Others help lenders calculate borrowing amounts and evaluate available home equity. One of the most common—and often misunderstood—is loan-to-value ratio, or LTV.

In traditional mortgage lending, LTV helps lenders evaluate risk, determine borrowing limits, and decide whether mortgage insurance is required. However, reverse mortgages work differently.

Rather than relying on traditional LTV requirements, reverse mortgages use several factors, including home value, available home equity, borrower age, and interest rates, to determine available proceeds. Understanding how LTV fits into that process may help you better evaluate your borrowing options and estimate how much home equity may be available through a reverse mortgage.

What is the reverse mortgage loan-to-value (LTV) ratio?

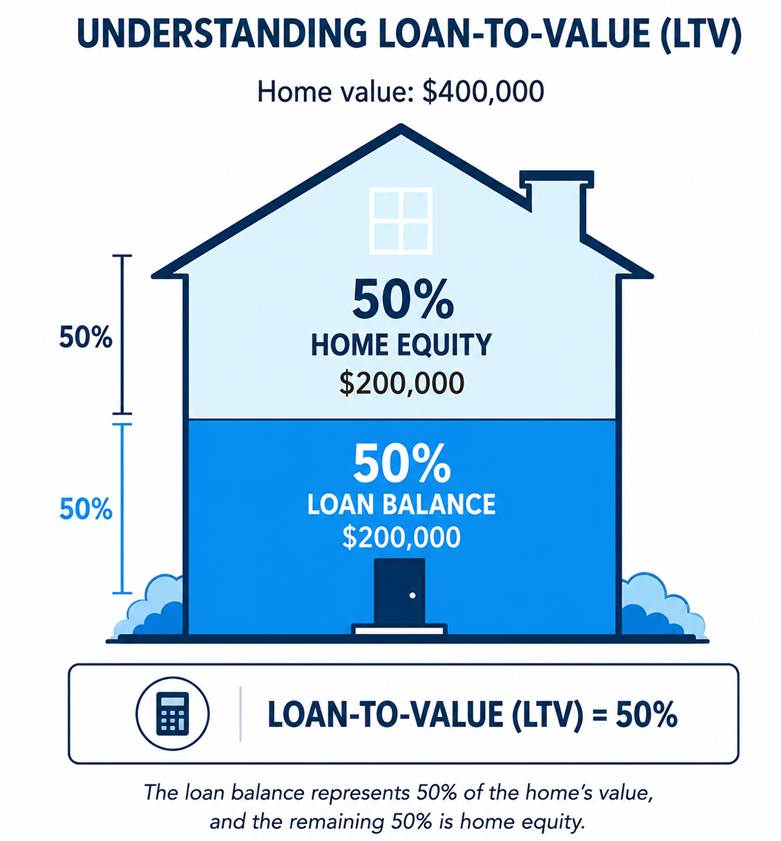

LTV ratio measures the relationship between a loan balance and a home’s value. A lower LTV generally means more home equity, while a higher LTV means a larger portion of the home’s value is tied to debt.

The formula to calculate LTV is:

Loan balance ÷ appraised home value × 100

For example, if you have a mortgage balance of $200,000 and your home is appraised at $400,000, your LTV is 50%. This means your loan balance represents 50% of your home’s value, while the remaining 50% is home equity.

In general, as LTV increases, homeowners have less home equity available in the property.

Because loan balances and home values change over time, LTV may change as well. Paying down a mortgage or rising home values may lower LTV, while increasing mortgage debt or declining home values may raise it.

How reverse mortgage LTV differs from traditional mortgage LTV

Before comparing LTV calculations, it may help to understand that there are two primary types of reverse mortgages: Home Equity Conversion Mortgages (HECMs), which are federally insured by the Federal Housing Administration (FHA), and proprietary reverse mortgages offered by private lenders. HECMs are the most common type of reverse mortgage and follow FHA program requirements, while proprietary reverse mortgages use lender-specific guidelines and may be available for higher-value homes.

While LTV is used in both traditional mortgages and reverse mortgages, the way lenders apply the concept is different.

With a traditional mortgage, LTV compares the loan amount to the home’s value and may influence factors such as interest rates, mortgage insurance requirements, and loan eligibility.

With a reverse mortgage, available proceeds generally depend on factors such as home value, available home equity, borrower age, interest rates, and the specific loan product.

| Feature | Traditional mortgage | Reverse mortgage |

| Primary purpose | Purchase or refinance a home | Access existing home equity |

| Down payment | Typically yes | No, unless using reverse mortgage for purchase |

| Key calculation | Loan amount relative to home value | Principal limit based on age, rates, and home value |

| LTV focus | Borrowing risk and financing | Available home equity and borrowing capacity |

Unlike traditional mortgages, HECM borrowing calculations are generally based on a principal limit—the maximum amount that may be available through the reverse mortgage—rather than a traditional LTV ratio. Proprietary reverse mortgages may use different underwriting and borrowing calculations depending on the lender and product.

To learn more, please visit the CFPB’s “Reverse Mortgage: A Discussion Guide.”

How principal limits and home equity affect reverse mortgage proceeds

A principal limit is the maximum amount that may be available through a HECM reverse mortgage or other reverse mortgage product. For HECMs, principal limits are determined using factors such as the age of the youngest borrower or co-borrower, home value, the expected interest rate, and applicable lending limits.

Because existing mortgage balances generally must be paid off at closing, a smaller current mortgage balance may leave more reverse mortgage proceeds available than a larger outstanding balance.

For example, Marcus and Carla both own homes worth $600,000. However, Marcus is 75 and has a small remaining mortgage balance, while Carla is 63 and owes more on her existing mortgage. Even though their homes have similar values, they may receive different reverse mortgage estimates because age, interest rates, and existing debt all affect their available proceeds.

→ Learn more about HECMs: What is a HECM loan and how does it work?

Principal limit vs. net principal limit

A principal limit represents the estimated loan advance that may be available through the reverse mortgage before deductions are applied.

The net principal limit is the amount remaining after those deductions are applied, such as:

- Existing mortgage payoffs

- Closing costs and fees

- Mortgage insurance premiums (for HECMs)

- Required set-asides, where applicable

- Other mandatory obligations

Because these costs vary from borrower to borrower, the net amount available may be lower than the initial principal limit.

Borrowing limits and the 60% rule

HECM borrowers are generally subject to limits on how much of the available proceeds they may access during the first year of the loan.

In many cases, borrowers may receive up to 60% of the available principal limit during the first 12 months. Additional funds may be available when required to satisfy existing mortgage balances or other mandatory obligations.

Understanding FHA lending limits

For HECM reverse mortgages, borrowing calculations are also subject to the FHA maximum claim amount.

In 2026, the FHA maximum claim amount is $1,249,125. This means HECM borrowing calculations are generally based on a home’s value up to that limit, even if the property is worth more.

Homeowners with properties that exceed the FHA lending limit may explore proprietary, or jumbo, reverse mortgage options offered by private lenders.

Why your estimate may differ

If you use an online reverse mortgage calculator, keep in mind that the estimate should be viewed as a starting point rather than a guaranteed loan amount. Final loan amounts are determined by the lender and may vary based on several factors, including the home’s appraised value, borrower age, interest rates, loan costs, and applicable product requirements.

What other factors influence reverse mortgage borrowing capacity?

Several factors may influence available reverse mortgage proceeds. Because every homeowner’s situation is unique, lenders generally consider the following:

| Factor | Why it matters |

| Age | Older borrowers may be eligible to access a larger portion of their home equity. |

| Interest rates | Higher rates may reduce available proceeds, while lower rates may increase them. |

| Home value | Higher-value homes may support larger borrowing amounts. |

| Existing mortgage balance | Larger mortgage balances reduce the amount of home equity available through the reverse mortgage. |

| Reverse mortgage type | HECMs and proprietary reverse mortgages use different product rules and lending limits. |

Because every homeowner’s situation is different, estimates may vary even when two homes have similar values.

→ Read more: How much can I get from a reverse mortgage?

What is combined loan-to-value ratio (CLTV)?

Combined loan-to-value ratio (CLTV) compares all loans secured by a property to the home’s value. Unlike traditional LTV, which looks at a single loan balance, CLTV accounts for multiple liens attached to the property.

The formula is:

CLTV = Total outstanding loan balances ÷ Appraised home value × 100

For example, if a homeowner has:

- A first mortgage balance of $150,000

- A home equity line of credit (HELOC) balance of $50,000

- A home value of $500,000

The CLTV would be:

($150,000 + $50,000) ÷ $500,000 x 100 = 40%

For reverse mortgage borrowers, CLTV may be relevant when existing mortgages, HELOCs, or other liens must be paid off as part of the loan process.

What is the 95% rule?

When a reverse mortgage becomes due and payable, borrowers and their heirs often have questions about repayment obligations and what happens if the loan balance exceeds the home’s value.

A reverse mortgage generally becomes due and payable when the last borrower dies, sells the home, permanently moves out of the property, or otherwise fails to meet the loan terms.

For federally insured HECMs, eligible heirs may have the option to satisfy the reverse mortgage by paying 95% of the home’s appraised value if the outstanding loan balance exceeds the home’s value.

For example, if a reverse mortgage balance grows to $450,000 but the home is appraised at $400,000 when the loan becomes due, eligible heirs may be able to satisfy the loan by paying 95% of the appraised value ($380,000) rather than the full $450,000 balance.

The 95% rule works together with the loan’s non-recourse feature, which generally protects borrowers and heirs from owing more than the home is worth, provided product requirements are met.1

Why understanding LTV matters

While reverse mortgages do not rely on traditional LTV requirements in the same way as forward mortgages, understanding LTV may help homeowners better evaluate available home equity and estimate potential reverse mortgage proceeds. It may also provide useful context for how factors such as age, interest rates, home value, and existing mortgage balances influence borrowing capacity.

If you’re interested in estimating how much may be available through a reverse mortgage, Finance of America’s reverse mortgage calculator may provide a helpful starting point. The calculator considers factors such as age, home value, and location to provide personalized estimates that may help you better understand your potential borrowing options.

FAQs

How is reverse mortgage LTV calculated?

Reverse mortgage LTV is calculated by dividing the loan balance by the home’s appraised value and multiplying the result by 100. The result is expressed as a percentage. For example, a 50% LTV means the loan balance is 50% of the home’s value.

Do reverse mortgages use LTV the same way traditional mortgages do?

No. While reverse mortgages consider the relationship between loan balances and home values, lenders typically focus more heavily on factors such as borrower age, available home equity, interest rates, and principal limits when determining available proceeds.

Does age affect reverse mortgage loan-to-value ratios?

Yes. For HECMs, lenders use the age of the youngest borrower when calculating available proceeds. In general, older borrowers may be eligible to access a larger portion of their home equity than younger borrowers. To be eligible for a HECM, borrowers generally must be at least 62 years old.

Do higher interest rates reduce reverse mortgage proceeds?

In many cases, yes. Higher interest rates generally reduce principal limit factors (PLFs), which may lower the amount available through a reverse mortgage.

How much home equity could you access with a reverse mortgage?

The amount available through a reverse mortgage depends on several factors, including age, home value, interest rates, existing mortgage balances, and loan type. Because every homeowner’s situation is different, available proceeds vary from borrower to borrower.

What is a good loan-to-value ratio for a reverse mortgage?

There is no universally good reverse mortgage LTV ratio. The right LTV depends on a homeowner’s borrowing needs, financial goals, and plans for the property.

Is a higher or lower LTV better for a reverse mortgage?

In general, a lower LTV means more home equity and may support greater reverse mortgage borrowing capacity. However, available proceeds also depend on factors such as age, interest rates, home value, and loan type.

What is the maximum LTV for a reverse mortgage?

There is no single maximum reverse mortgage LTV that applies to every borrower or loan product. Available borrowing amounts vary based on factors such as age, home value, interest rates, loan type, and product requirements. For HECM loans, available proceeds are determined using principal limit calculations rather than a fixed maximum LTV.

Can you get a reverse mortgage if you still have a mortgage balance?

Yes. In most cases, the existing mortgage balance must be paid off using reverse mortgage proceeds at closing. Because the payoff amount reduces available home equity, homeowners with larger mortgage balances may have less available proceeds than those who owe less or own their homes outright.

Does a reverse mortgage use combined LTV (CLTV)?

In some situations, yes. CLTV may be used when multiple liens or loans are secured by the property because it considers the total balance of all secured debt.

What happens if the reverse mortgage balance exceeds the home’s value?

For federally insured HECMs, borrowers and heirs are generally protected by the loan’s non-recourse feature. This means they are not personally liable for any difference between the loan balance and the home’s value when the loan becomes due, provided product requirements are met.1

What is the 95% rule for reverse mortgages?

When a HECM becomes due and payable, eligible heirs may have the option to satisfy the loan by paying 95% of the home’s appraised value if the loan balance exceeds the home’s value.

1Non-recourse means that you, or your estate, can’t owe more than the value of your home when the loan becomes due and the home is sold.

Non-recourse means that if you default on the loan, or if the loan cannot otherwise be repaid, the lender cannot look to your other assets (or your estate’s assets) to meet the outstanding balance on your loan.

About the author

is a Senior Web Content Writer at Finance of America and a journalist with more than 20 years of experience specializing in business, and technology. Her work has been published in The Wall Street Journal, The Financial Times, and numerous other leading outlets.

Disclaimer

This article is intended for general informational and educational purposes only and should not be construed as financial or tax advice. For tax advice, please consult a tax professional. For more information about whether a reverse mortgage fits into your retirement strategy, you should consult your financial advisor.